DSCR vs Conventional Loan: Which Is Right for Real Estate Investors in 2026?

July 9, 2024

Conventional mortgages follow guidelines built around personal income and owner-occupied properties. They carry structural limitations that become potential problems when applied to investment properties, including W-2 and tax return requirements, debt-to-income (DTI) ceilings, a hard cap on how many properties you can finance, and restrictions on holding title in an LLC.

DSCR loans are built for real estate investors holding rental properties. Qualification is based on what the property rental income is, not what the borrower earns personally. That makes DSCR loans the go-to financing structure for investors at almost every stage — whether it's your first rental property acquisition or you’re growing a real estate portfolio.

This guide compares both conventional loans and DSCR loans side by side and explains when investors should consider using each product.

What Is a DSCR Loan?

A DSCR loan is a type of investment property financing that qualifies borrowers based on a property's rental income rather than the borrower's personal income. DSCR stands for Debt Service Coverage Ratio — a metric used by lenders to measure whether a property's gross rental income is sufficient to cover its monthly debt obligation.

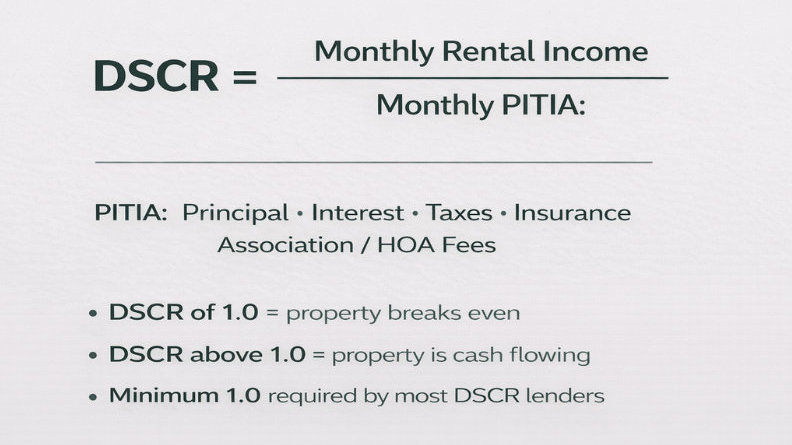

How DSCR is calculated

The formula compares monthly rental income against the property's total monthly debt payments, specifically PITIA: Principal, Interest, Taxes, Insurance, and any applicable Association or HOA fees.

DSCR = Monthly Rental Income ÷ Monthly PITIA

A DSCR of 1.0 means the property breaks even — rental income exactly covers the debt payment. A DSCR above 1.0 means the property is cash flowing. Most DSCR lenders require a minimum ratio of 1.0 to qualify. Use our DSCR calculator to run numbers on your property.

Why Investors Use DSCR Loans for Rental Properties?

DSCR loans have become very popular for rental property investors and are becoming the prevailing choice for investment properties for investors who are aware of the advantages they provide.

Conventional underwriting consistently excludes or limits certain borrowers. DSCR loans were built to serve exactly those investors:

- Self-employed borrowers whose tax returns understate actual income due to legitimate deductions

- Short-term rental operators who can't meet conventional lenders' two-year income history requirement

- Investors who hold properties through an LLC and need a loan structure that matches their ownership from day one

- Foreign nationals without U.S. employment history

DSCR also solves a scaling problem conventional financing creates. Each conventional loan adds to personal DTI and moves the borrower closer to the 10-property ceiling. DSCR carries no DTI calculation and no property count limit.

What Is a Conventional Loan?

A conventional loan is a traditional mortgage that follows guidelines set by Fannie Mae or Freddie Mac. It is not insured by a government agency. Other programs — FHA, VA, and USDA loans — are insured by the government in cases of default, which is what separates them from conventional financing. Conventional loans are most commonly used for primary residences, but are also available for investment properties, often for investors who haven't yet fully explored rental property financing options.

Conventional loan approval is borrower-centric: lenders focus on the personal financial profile of the borrower, including W-2 income, tax returns, employment history, and personal debt obligations.

Why Investors Use Conventional Loans for Rental Properties In Some Cases

For many investors, conventional financing is simply the path of least resistance. They used it to buy their primary residence, they understand how it works, and reaching for the same product to finance a rental feels like a natural next step. For borrowers with a strong W-2 income and a high FICO credit score, qualifying is straightforward, and the interest rate will be lower than that of a DSCR loan.

What most of those investors underestimate is the structural limitations that come with conventional financing on investment property. Rental debt reports to personal credit. Title must be held in a personal name, not an LLC, which means the borrower is personally exposed in any liability scenario. Every new mortgage adds to personal DTI, compressing the capacity to finance the next property. And Fannie Mae caps the total number of financed properties at 10, with many banks applying a stricter limit of 4. Those constraints are easy to ignore on the first acquisition. They become significant by the third or fourth.

Investors with high income and high FICO scores sometimes choose conventional loans for the rate. Sophisticated real estate investors typically choose DSCR from the first investment deal, for the entity protection, the qualification flexibility, and the ability to scale without a ceiling.

Key Differences Between DSCR and Conventional Loans

DSCR loans and conventional loans differ primarily in how borrowers qualify, underwriting flexibility, and investor scalability for purchasing multiple properties. The table below highlights the most important differences.

DSCR vs. Conventional Loans: Side-by-Side Comparison

DSCR Loans vs. Conventional Loans: Pros and Cons.

We have a full breakdown of DSCR Loan Pros and Cons in this guide, but here are the 5 differences that matter most:

Qualification. DSCR loans require no personal income documentation. Conventional loans require W-2s, tax returns, and a DTI calculation that accounts for every debt obligation the borrower carries. For self-employed investors, LLC borrowers, and anyone with a complex income structure, this is the key factor.

Scalability. Conventional loans count toward personal DTI and carry a hard cap of 10 financed properties. DSCR loans carry no DTI calculation and no property count ceiling. Each acquisition qualifies on its own cash flow, independent of what the borrower holds elsewhere.

Rates. Conventional loans are priced lower — typically 0.5% to % less than a comparable DSCR loan for qualified borrowers.

Prepayment penalties. Conventional loans carry none. DSCR loans typically include a step-down penalty — commonly 5-4-3-2-1, meaning 5% of the loan balance if paid off in year one, declining by 1% each year. Investors who plan to sell or refinance within five years need to factor that cost into the return analysis before closing.

Liability and credit protection. DSCR loans keep rental debt off your personal credit report and support LLC ownership. Conventional investment loans require personal title and report to personal credit bureaus..

Why Real Estate Investors Switch to DSCR Loans

For investors who started with a conventional mortgage, two mechanics accelerate the ceiling faster than expected.

The first is the rental income vacancy discount. Conventional lenders don't count the full rent from an investment property. Fannie Mae requires a 25% reduction before applying rental income to the DTI calculation — accounting for vacancy and maintenance. A property renting for $2,000 per month contributes $1,500 toward the borrower's income picture. Every new property added to the portfolio is treated as a full mortgage obligation against personal income, but only 75% of its rent counts back. The DTI looks tighter with each acquisition than the actual cash flow provides.

The second is the property count ceiling. Fannie Mae caps borrowers at 10 financed properties. Many retail banks apply an internal limit of 4. Once that ceiling is reached, no amount of income, credit, or down payment opens the door to another conventional loan.

DSCR eliminates both. Each acquisition qualifies on its own income, gross rent at full value, with no ceiling on portfolio size.

Which Loan Is Better for Real Estate Investors?

Now that you have a clear picture of the differences between DSCR and Conventional loans, you might be wondering whether or not a DSCR loan is the right product for your situation.

Here are the common investor profiles for DSCR Loan borrowers:

How to get a DSCR Loan with Ridge Street Capital

Ridge Street Capital is an investment-property-only lender across 35 states, focused exclusively on real estate investors. We finance single-family homes and 2–10 unit residential properties, including long-term rentals and Airbnb loans.

What separates Ridge Street from most DSCR lenders is the combination of low origination fees and fast execution. To get started, investors can get pre-approved for a DSCR loan through Ridge Street's online application. After submission, a Ridge Street loan officer reaches out to verify property details and deal structure. The team then runs the numbers and issues a term sheet or pre-approval letter within 2 business hours. From there, the process moves toward closing with direct lender support at each stage.

DSCR vs. Conventional Loans FAQs

Do credit scores affect DSCR loan qualification?

Yes, credit scores still matter for DSCR loans. They affect pricing and program eligibility, not the income qualification method. Most DSCR lenders require a minimum score in the 660–680 range. Higher scores result in better rates. The key difference from conventional loans is that the credit score affects how the loan is priced, not whether the property's income qualifies. A strong-cash-flowing property with a borrower at 700 credit will qualify; the same property will simply be priced differently than it would be at 760.

How does the prepayment penalty on a DSCR loan work?

Most DSCR loans include a step-down prepayment penalty, typically structured over three to five years. A common structure is 5-4-3-2-1: if the loan is paid off or refinanced in year one, the penalty is 5% of the outstanding balance; year two is 4%; and so on until the penalty period expires. Investors who anticipate selling or refinancing within a few years should factor this cost into the return analysis before closing. Conventional loans generally carry no prepayment penalty.

Can a short-term rental property qualify for a DSCR loan?

Yes. Ridge Street Capital uses AirDNA data to project rental income for the property when underwriting DSCR loans for Airbnb. Conventional loans typically require two years of documented rental income history on tax returns, which makes them harder to use for STR acquisitions without an established operating track record.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)