DSCR Loan Explained: The Complete 2026 Guide

October 9, 2025

A DSCR loan is a rental property loan that qualifies the borrower based on the property's cash flow, not personal income. DSCR stands for Debt Service Coverage Ratio — the ratio that compares a property's monthly rental income to its monthly debt obligations. When that ratio is 1.0 or higher, the property qualifies. The borrower's W-2s, tax returns, and employment history are not part of the evaluation.

For real estate investors, that distinction is significant. Most investors scaling a rental portfolio, whether long-term or short-term, face a common ceiling: conventional financing is based on personal income and caps the number of financed properties. DSCR financing removes both constraints. Each property qualifies on its own cash flow, independent of what the investor already owns or earns.

For most real estate investors, three factors matter most when choosing a lending partner:

- Cost of financing (rates and fees)

- Closing time and efficiency

- Reliability of execution

This guide covers all three. It starts with the fundamentals: what DSCR loans are, how the ratio is calculated, and how income is evaluated, then moves through rates, requirements, refinancing, LLC structure, and the step-by-step process from application to close.

DSCR Loans Explained: How They Work

A DSCR loan is a type of investment property financing that qualifies the borrower based on the property's cash flow, instead of the borrower's personal income. DSCR loans are a type of non-QM (non-qualified mortgage) loan, meaning they operate outside Fannie Mae and Freddie Mac guidelines.

DSCR stands for Debt Service Coverage Ratio — a financial ratio comparing a property's rental income to its monthly debt obligations, property taxes, insurance, and HOA fees where applicable.

Where:

- Rent = Actual Rent Collected (Appraiser’s Market Rent OR AirDNA Short Term Rent Projection)

- Monthly Debt Service = PITIA = Principal + Interest + Taxes + Insurance (+ Association dues, if applicable)

Why DSCR Matters?

DSCR matters because it demonstrates that a property's rental income covers the cost of ownership. A ratio above 1.0 means the property generates more income than it costs to carry. A ratio below 1.0 means the debt service exceeds the rental income — the property is cash-flow negative, and most lenders will not finance it on a DSCR program.

From the lender's perspective, DSCR establishes that the loan can be serviced from the property itself, without relying on the borrower's personal income to cover shortfalls. That is what makes DSCR financing distinct from conventional investment property loans.

DSCR Loan Explained on a Real Example

The example below walks through a real rental property in Texas to show how the ratio is calculated in practice.

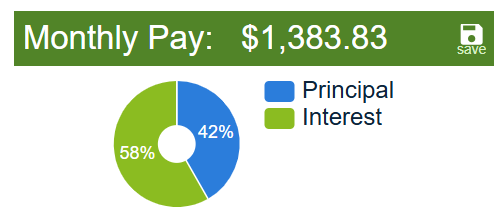

Purchase Price: $260,000 (example property on Zillow).

Estimated Rent: $2,134/month (using Zillow Rental Estimator; final figure determined by appraisal).

Taxes: $5,789/year or $482.42/month (from Zillow tax history).

Insurance: Conservatively estimated at 1% of purchase price = $2,600/year or $216.67/month

P&I Payment: At 7.0% interest, 30-year fixed, loan amount $208,000 (80% LTV) → $1,383.83/month.

Monthly Breakdown:

- Rent = $2,134

- Monthly Debt Service = $1,383.83 + $482.42 + $216.67 = $2,082.92

- DSCR = $2,134 ÷ $2,082.92 = 1.025 ✅ Passes DSCR requirement

The DSCR ratio of the property is above 1, which means the property will cash flow and will qualify for a DSCR loan. To analyze and calculate the DSCR ratio on prospective investment properties, use our DSCR Calculator.

DSCR Loans vs. Conventional Loans

Understanding how DSCR loans differ from conventional financing helps investors identify which path fits their situation. The comparison below covers the key structural differences.

Key takeaway: Conventional loans offer lower rates for investors who qualify on personal income. DSCR loans remove the income and property count constraints, which makes them the standard vehicle for investors scaling beyond two or three properties. For a full comparison, see the DSCR vs. Conventional Loan guide.

Who Should Use a DSCR Loan

DSCR loans serve investors whose deals do not fit conventional underwriting, because income is difficult to document, because they have reached the limits of conventional financing, or because the deal requires entity ownership or a fast close.

- Self-employed investors and those with complex tax situations qualify on the property's cash flow rather than reported personal earnings.

- Portfolio investors who have reached debt-to-income (DTI) limits or the Fannie Mae property count cap use DSCR to continue acquiring without personal income constraints.

- BRRRR investors refinancing out of a hard money loan use DSCR to convert short-term bridge debt into long-term financing once the property is stabilized and rented.

- Investors acquiring short-term rental properties use DSCR programs that evaluate income on AirDNA projections rather than long-term lease assumptions.

- Investors closing on a competitive acquisition use DSCR lenders who can execute in 21 to 25 days rather than the 45 to 60-day conventional timeline.

Benefits of DSCR Loans

- No personal income verification: qualification is based on the property's rental income, not W-2s or tax returns.

- No limit on the number of financed properties: each acquisition qualifies independently on the property's own DSCR ratio.

- LLC-eligible from the first transaction: DSCR loans close in the name of an entity and do not report to the borrower's personal credit bureaus.

- Available to first-time rental property investors: prior investment property ownership is not required.

- Works for both long-term and short-term rentals: income is evaluated on appraiser market rent for LTR and AirDNA projections for STR.

DSCR Rates Explained

This section covers how DSCR loan rates are determined and how to check an estimated rate for a specific deal.

Understanding How DSCR Rates Are Determined

Interest rates for DSCR loans are not arbitrary, they are tied two two factors:

1. Industry Benchmark Rates for other Long Term Debt Products,

2. Risk Of Default Premiums.

DSCR rates are determined using the following formula:

The U.S. 2YR Treasury Index is the rate at which the U.S. government lends money (via Bonds) on a 2 Year Term. This is considered the Base Rate (Risk Free Rate) for most debt offerings. As such, this index is used as a benchmark for DSCR Loan Rates - i.e. as the US 2 YR Treasury Bond Yield falls, so do DSCR Loan Rates. You can check the current Base Rate Index here: U.S. 2 YR Treasury Yield.

DSCR lenders then add a risk premium to the base rate. The premium is determined by:

- Credit score

- Loan-to-Value (LTV)

- Property type

- Long-term rental vs. short-term rental

- Transaction type: purchase vs. cash-out refinance

- Amortization type: fully amortizing vs. interest only

- DSCR ratio

Example Of DSCR Rate Calculation

The example above outlines how different factors affect the final DSCR loan rate. It is important to mention that the actual premiums that DSCR Lenders use to calculate the rates of DSCR loans are proprietary. To get a formal quote on a DSCR loan scenario, you can request a Term Sheet here: Get A DSCR Loan Quote.

Understanding DSCR Loan Amortization and Interest-Only Options

Standard DSCR Loans are fully amortizing over 30 years. This means, every month the mortgage payment goes towards paying down the principle balance and towards paying the interest of the loan.

In some cases, investors will chose to have a DSCR Loan with an interest only period for the first 10 years in exchange for a lower payment and a slightly higher interest rate. By not paying down the principle of the loan, the monthly DSCR loan payment becomes lower. This interest only option is considered to be a slightly higher risk loan, so the interest rates are higher than the standard fully amortizing DSCR loans.

DSCR Loans for Cash Out Refinances

DSCR loans are commonly used for refinancing rental properties either to obtain a lower rate or to pull equity from a stabilized asset (a.k.a. “cash out”).

The two types of refinance transactions are:

- Rate & Term Refinance: Replace an existing mortgage with better terms.

- Cash-Out Refinance: Obtain leverage on a property by borrowing more than you owe. Rates are usually slightly higher for cash-out refinance (≈0.20%) because lenders view it as slightly riskier.

With refinances, the same qualification logic applies: the property's rental income must cover the new monthly debt service at a DSCR of 1.0 or higher.

Use our DSCR refinance calculator to run the numbers for your deal.

Important Notes About Refinancing With A DSCR Loan

- When ever you finance a property, you will pay closing costs including the cost of title work, an Appraisal, and Taxes & Insurance escrows.

- For Rate & Term Refinances, the maximum leverage on a DSCR loan is 80%. On a Cash Out Refinance DSCR Loan, the maximum leverage available is 75% of the appraised value.

- Leverage (LTV %) is calculated based on the appraised value of the property.

How DSCR Loans Work with the BRRRR Strategy

If you’re reading this guide, you may have heard the term: BRRRR — which stands for Buy, Rehab, Rent, Refinance, Repeat. This is an investment strategy where real estate investors buy a distressed property, renovate it, and then refinance/cash out the property based on the new value and cashflow. The BRRRR Strategy is extremely popular because, when it’s done right, investors can obtain a rental property and regain the initial cash they invested in the project at the completion of the BRRRR project. This makes it a very scalable strategy for investors to obtain 1-2 properties per year.

BRRRR Project Example:

-min.png)

Overview:

- An investor bought a distressed single family home for $285K using a fix and flip loan (also called a hard money loan).

- $90,000 of renovations were completed over 6 months.

- The property then was rented for $3,600/month.

- The propety appraised for $525,000.

- The project was then refinanced with a Cash Out DSCR Loan at 75% LTV for a total loan amount of $393,750.

- With the DSCR loan in place, the monthly cashflow of the property looks like this:

- Rent: $3,600

- Principle & Interest Payment: $2,659.42

- Monthly Taxes: $330

- Monthly Insurance: $360

- Net Operating Income: $250.58

Again, since the DSCR loan covered the cost of the original purchase plus renovation, the borrower was able to obtain a long term rental property and recoup their initial investment.

If you want to analyze pontential BRRRR Investments that you’re considering, we created this BRRRR Calculator to help with your analysis.

Seasoning Requirements When Refinancing With A DSCR Loan

Cash-out refinances on DSCR loans have a seasoning requirement when the loan amount exceeds what the investor originally put into the deal. If the refinance pulls out more than the original purchase price plus renovation costs, a 6-month waiting period from the original purchase date applies. If the refinance only recovers those original costs, no seasoning period is required.

Closing a DSCR Loan in an LLC

DSCR loans can be closed in an LLC or in the investor's personal name. Most investors holding rental properties in an LLC use DSCR financing as the standard path, since conventional loans require a personal name on the title. The key points:

- Ownership structure: DSCR loans support both personal name and LLC ownership in most states.

- Required LLC documents at closing: Articles of Formation, Operating Agreement, EIN, Certificate of Good Standing, and a business bank statement.

- Credit reporting: DSCR loans closed in an LLC do not report to the guarantor's personal credit bureaus. Conventional investment property mortgages do report to personal credit, which is one reason investors refinance out of conventional financing into DSCR as their portfolio grows. This helps investors avoid credit utilization penalties and helps maintain FICO Scores, which is a common issue with conventional financing on investment properties.

For a full breakdown of how DSCR loans work under an LLC see the dedicated DSCR loan for LLC guide.

DSCR Loan Process Explained

The process for closing a DSCR Loan varies by Lender. Standard DSCR Lenders take 30-45 days to closing. The best DSCR lenders can close in 21-25 days.

Below is a step-by-step overview of each stage in the DSCR Loan Process:

1. Pre-Screening. Before applying, investors should pre-screen the property to confirm it may be eligible for DSCR financing. Ridge Street's DSCR Calculator provides a quick check.

2. Request Term Sheet or Pre-Approval. Once the deal looks viable, investors can request a formal quote (term sheet) directly through Ridge Street's application.

3. Get Property Under Contract. For purchases, the investor makes an offer and obtains an executed purchase contract. Refinances skip this step.

4. Complete Loan Application and Pay Appraisal Invoice. The formal application collects personal information, credit is pulled, and an appraisal is ordered. The quoted rate locks for 45 days once the appraisal is ordered.

5. Collect Documentation. Required documents:

- Photo ID,

- Bank statement,

- Entity documents (if LLC),

- Rental contract (if refinance),

- Voided check. No personal income verification is required

6. Quality Control Review. Once the appraisal is returned, the file moves to internal QC review. The team verifies documents, confirms cash to close, and checks entity documents.

7. Schedule Closing. Closing is typically scheduled 2 to 3 days after formal approval.

8. Funding. On closing day, documents are signed in person at the title office or via mobile notary. Funding happens within 24 hours of the lender receiving the executed loan package from the title company.

Requirements to Get a DSCR Loan

Below is checklist for the borrower requirements, property requirements, and document requirements needed for a DSCR Loan.

Borrower Requirements

- Credit Score: 660+

- No mortgage lates in past 24 months

- Liquidity: Down Payment + Closing Costs + 6 Months PITIA

- First-time investors allowed

- Individual or LLC borrower

- U.S. Citizen or Permanent Resident

Property Requirements

- Property type: 1–4 unit residential or small multifamily (5–10 units)

- DSCR > 1.0

- Property must be rent-ready

- Vacant properties permitted

Document Checklist

- Photo ID

- Bank Statement

- Entity Documents (if LLC)

- Appraisal (ordered by lender)

- Completed Loan Application

DSCR Loan Pros and Cons

DSCR loans have become the standard financing vehicle for investors scaling a rental portfolio — no property count limit, no personal income requirement, and LLC-eligible from the first acquisition. Like any loan product, they come with tradeoffs. The main drawback is cost: DSCR loans carry higher rates than conventional investment property loans and require a minimum 20% down payment. For investors where the flexibility outweighs the rate premium, the economics typically work. For a full breakdown of how these tradeoffs play out across different strategies and deal types, see the DSCR loan pros and cons guide.

DSCR Loans for Long-Term vs. Short-Term Rentals

Short-term rentals have grown significantly in popularity because of their ability to generate higher revenue than long-term rentals in the same market. In many cases, the short-term rental strategy is what makes a property cash-flow positive in markets where long-term rents would not support the debt service.

On the financing side, DSCR for short-term rentals is sometimes referred to as DSCR loans for Airbnb, Airbnb loans, or short-term rental loans — all referring to the same loan product. The key difference from long-term rental DSCR is how income is evaluated: for STR, the qualifying income comes from AirDNA projections rather than appraiser market rent. AirDNA is a data analysis tool that aggregates short term rental history from Airbnbs across the U.S. and makes a projection about a property based on the comparable properties with similar specifications.

Below is comparison of DSCR Loans for Long Term Rentals and DSCR Loans for Short Term Rentals:

Long-Term Rentals (LTR):

- Rent determined by appraiser’s market rent.

- No landlord experience required.

- Slightly lower interest rates.

Short-Term Rentals (STR):

- Cash flow estimated with AirDNA cashflow projection.

- Require some real estate experience (1 other rental or a personal mortgage).

- Slightly higher rates (≈+0.25%).

- Higher income potential but more management intensive.

DSCR Loan Case Studies

The three funded deals below show how investors used DSCR financing in some of the best states for rental property investment, across different property types and investment strategies.

Case Study 1: DSCR Loan Purchase Transaction

This first time investor purchased a single family rental property in Memphis, TN with DSCR loan. Below is a breakdown of the relevant transaction figures:

- Purchase Price: $118,000

- Appraised Rent: $1,200/month

- Loan Amount: $94,400 (80% LTV)

- Rate: 7.375%

- Taxes: $1,200/year

- Insurance: $1,180/year

- P&I: $652/month

- DSCR = 1.41

Case Study 2: DSCR Cash-Out Refinance (Portfolio)

This experienced real estate investment power couple, used a DSCR Loan to cash out refinance 6 of their properties so that they could obtain more real estate with the cash out proceeds. See the relevant transaction details below:

- Appraised Portfolio Value: $1,653,000

- Total Actual Rent: $13,200/month

- Loan Amount: $1,240,000

- Rate: 7.75%

- Total Annual Taxes: $31,405/year

- Total Annual Insurance: $19,615/year

- P&I Payment: $8,883

- DSCR: 1.00

Case Study 3: Airbnb Purchase Transaction

This first time Airbnb investor purchased this cabin in New Hampshire, with a DSCR loan. See the deal figures below:

- Purchase Price: $725,000

- AirDNA Revenue Estimate: $71,000/year

- Loan Amount: $580,000

- Rate: 7.275%

- Annual Taxes: $3,760/year

- Annual Insurance: $2945/year

- P&I Payment: $3,996/month

- DSCR = 1.30

Closing Costs in DSCR Loans

As we close out this guide on DSCR Loans, its time that we talk about the closing costs of a DSCR loan.

Standard Costs Include:

- Appraisal. Appraisal costs are typically between $600-$750 depending on the location of the property.

- Title & Escrow fees. Whenever, a property is financed a Lender’s Title Insurance Policy will have to be obtained. On small loans, title insurance costs about $1,000 and on larger loans over a million dollars, a title insurance policy typically costs $3,000-$4,000. Additionally, the actual title company typically charges $500-$1,500 for there services.

- Recording fees. Whenever you get a Mortgage (DSCR Loan), that document is recorded in the county where the property is located. Typically, county recording fees are $100-$400.

- Lender fees. On a DSCR loan, there are two types of Lender Fees: 1. Origination Fee and 2. Legal/Underwriting Fees. Some DSCR lenders, like Ridge Street Capital, offers DSCR loans with 0% Origination Fees but most DSCR Lenders charge 1-2% of the loan amount. Then, there is a standard $1,995 Legal and Underwriting Fee on most DSCR Loans.

- Prepaid Taxes & Insurance Escrow. The lender collects 2 to 3 months of taxes and insurance at closing as an escrow cushion, in addition to the monthly tax and insurance amounts that roll into PITIA going forward.

Then there are two other types of fees that may be present in a DSCR loan transaction based on the region — the two types of fees are: transfer tax and mortgage tax.

- Transfer Tax. Most states do not impose a transfer tax on real estate purchases. States including Pennsylvania and Massachusetts charge 0.5% to 2% of the purchase price, split between buyer and seller.

- Mortgage Tax. Most states do not impose a mortgage tax. New York and Maryland are notable exceptions, with rates between 0.25% and 1.5% of the loan amount.

How To Apply for a DSCR Loan

To apply, investors submit a quick application or pre-approval form through Ridge Street's Get Started page. A loan officer reviews the deal, runs the numbers, and issues a term sheet within 2 business hours.

DSCR Loans Explained FAQ

Can I get a DSCR loan under $100K?

Yes, some lenders finance properties below $100,000. Ridge Street Capital finances properties valued at as little as $75,000 with loan amounts from $55,000.

What is the minimum DSCR ratio for approval?

A Debt Service Coverage Ratio of 1.0 is required by most DSCR lenders, including Ridge Street Capital.

Can foreign nationals qualify?

Some lenders allow foreign nationals with higher down payments. Ridge Street does not lend to foreign nationals without permanent U.S. residency.

How fast can a DSCR loan close?

The typical timeline is 3 to 4 weeks with documents and appraisal ready. Ridge Street closes most loans in 21 to 25 days.

Are prepayment penalties common?

Yes. Most DSCR loans include a prepayment penalty, typically a step-down structure over 3 to 5 years. 0-year and 1-year prepayment options are also available.

Can self-employed investors or investors with low taxable income qualify?

Yes. Qualification is based on the property's cash flow, not personal income. Tax returns and W-2s are not required.

What property types are eligible?

The following property types are eligible:

• Single-family residential

• 2–4 unit residential

• 5–10 unit multifamily

Are DSCR loan rates higher than conventional rates?

DSCR loan rates are typically 0.25% to 0.5% higher than conventional investment property rates. The difference reflects the no-income-documentation structure and the non-QM classification.

What happens if the DSCR changes over time?

DSCR loans are underwritten at origination based on the conditions at the time of financing. As long as payments are made on time, no changes to loan terms are triggered by changes in the property's operating income after closing.

Final Comments On DSCR Loans

DSCR loans are one of the most powerful tools for scaling a rental property portfolio. By qualifying based on property income rather than personal income, they allow investors to:

- Acquire more properties without hitting conventional loan limitations.

- Structure deals in LLCs for liability and credit separation.

- Pursue both LTR and STR investment strategies.

Whether you’re looking to purchase, refinance, or cash out, understanding DSCR is the key to unlocking growth in your real estate business.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)