DSCR Loan Requirements: What Investors Need to Qualify

November 15, 2025

A DSCR loan is a type of investment property financing that qualifies real estate investors based on a property’s rental income rather than personal income verification.

The debt service coverage ratio (DSCR) is used to measure whether that income is sufficient to cover monthly mortgage payments, operating expenses, and other debt obligations.

However, there are other requirements involved with a DSCR Loan that can vary widely between lenders, states, and property types.

In this guide, we’ll break down all DSCR loan requirements by:

- Property type (Single-Family, 2–4 Units, 5–10 Units, STR/LTR)

- Borrower financial requirements

- DSCR ratio calculation

- Down payment & reserve rules

- State-specific exceptions

- LLC eligibility

- What investors can do to qualify faster

If you want the clearest, lender-accurate breakdown of how DSCR qualification works, this is the best place to start.

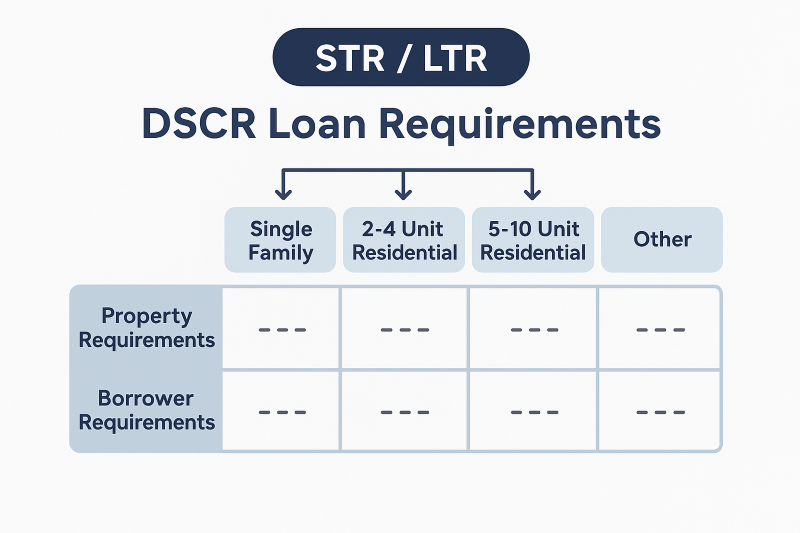

What Are The Requirements For A DSCR Loan?

Lenders assess DSCR loans using measurable criteria tied to the property’s income and overall risk profile. The requirements for a DSCR Loan vary depending on the investment strategy (Long Term Rental vs. Short Term Rental) and by the property type (Single Family, 2-4 Unit Residential, and 5-10 Unit Residential).

Unlike traditional mortgages that rely on your tax returns, pay stubs, and personal income, DSCR loans are approved based primarily on the property’s cash flow. This means lenders have less borrower income requirements and care more about whether the property can comfortably cover its own debt payments. The following are the main qualification standards for DSCR loans:

Standard DSCR Loan Requirements (Long Term Rental, 1-4 Unit Properties)

DSCR Loan Requirements for STR's (Short Term Rental, 1-4 Unit Properties)

Multifamily DSCR Loan (Long Term Rental, 5-10 Unit)

How Lenders Calculate the DSCR Ratio

Lenders use the debt service coverage ratio (DSCR) to determine whether a property’s income is sufficient to cover its debt obligations. The ratio compares net operating income (NOI) to total debt service, which includes the monthly mortgage payment, property taxes, insurance, and HOA fees.

DSCR = Net Operating Income ÷ Total Debt Service

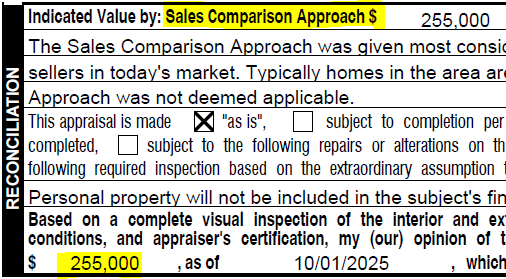

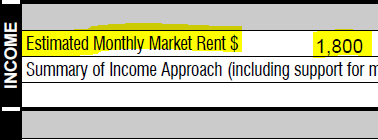

On purchase transactions, most properties acquired with a DSCR loan will be vacant. In this case, the rental income number used in the DSCR calculation will be the “Appraised Market Rent”. When you purchase a property with a DSCR Loan, the property will always be appraised. In the Standard Residential Appraisal Form (Form 1004 D), there will be a Market Sale Value and a Market Rental Value.

| Appraisal Valuation Type | Actual Appraisal Example | Details/Notes |

|---|---|---|

| Sales Price Valuation |  |

Appraised value of the property based on sold comparables. |

| Market Rental Valuation |  |

Appraised monthly rental value of the property based on rented comparables. |

In cases where the property is being cash-out refinanced, the actual current rental value is used in the DSCR calculation.

Are There Any State Level DSCR Loan Requirements?

The requirements for DSCR loans are consistent across most states. There are some minor DSCR loan requirement differences for a few states.

Pre-Payment Penalty Requirements For DSCR Loans

Most DSCR Loans have a pre-payment penalty (PPP) within the first 1-5 years.

For example, a 5YR PPP would have a declining structure of 5/4/3/2/1, where a 5% penalty would be imposed if the DSCR loan was paid off in the first year, a 4% penalty if paid off in the second year, continuing on until after the 5th year where there would be no penalty for paying off the loan early.

Some States specifically prohibit or restrict the PPP’s on DSCR loans. These states include:

In these states, the pre-payment penalty restrictions typically result in a slightly higher interest rate of +0.5% to +1.0%. Ultimately, this is not a deal-breaker for real estate investors but something to be aware of when you work with a DSCR Lender.

Flood Insurance Requirements For DSCR Loans

Most states for rental property investment don’t require rental properties to be insured with Flood Coverage. However, some coastal regions in high flood risk areas require a flood policy. Coastal regions of Florida, Texas, Alabama, Mississippi, etc, should be checked for a flood zone.

If you want to check if your property is in a flood zone, the FEMA Flood Map Service has a great free tool for checking whether or not your property is in a flood zone.

LLC Requirements For A DSCR Loan

In most states, a DSCR Loan can be closed in a borrower’s personal name or in an LLC. However, the following states specifically require that a DSCR loan be closed in an LLC:

- Georgia

- Hawaii

- Massachusetts

- New Jersey

- New York

- Pennsylvania

- Virginia

Our guide to DSCR loans for an LLC, go through the steps and process for setting up and closing a DSCR mortgage in an LLC.

What Documents Are Required For A DSCR Loan?

DSCR Loans require less documentation than a standard conventional mortgage. Below we’ve created a DSCR Loan Checklist to help you make sure you have everything you need for your DSCR Loan application:

DSCR Loan Document Requirements Checklist

If you have the documentation above, you can get pre-approved for a DSCR loan with Ridge Street.

Factors that Strengthen Your DSCR Loan Application

While DSCR loan requirements set the baseline for loan eligibility, certain factors can improve your DSCR loan interest rate and loan terms. Lenders reward strong financial indicators and well-performing properties because they lower overall portfolio risk.

- Higher DSCR Ratio: A DSCR above 1.20 signals that the property generates sufficient income to cover debt payments and operating expenses. These stronger DSCR ratio properties result in a lower rate.

- Strong Credit Profile: Stronger credit scores command lower interest rates. Credit scores at the bottom of the acceptable credit score range (660-680) will have the highest interest rates with scores above 760 commanding the lowest interest rates. DSCR loan interest rates improve every 20 FICO points. See an example in our guide on DSCR loan credit score requirements.

- Larger Down Payment: Investors who contribute 25–30% equity reduce the lender’s exposure and improve their loan terms. A higher down payment will command lower interest rates.

Common DSCR Loan Terms

While every lender structures investment property loans differently, most DSCR programs share similar terms and conditions. These determine how the loan performs over time and how much cash flow the property retains each month.

Key Takeaways

- DSCR loans offer flexible structures that prioritize cash flow and portfolio scalability.

- Interest-only payments and longer amortization terms help real estate investors maintain liquidity.

- Understanding rate adjustments and prepayment penalties is essential before finalizing any mortgage loan.

Is a DSCR Loan Right for You?

A DSCR loan is designed for real estate investors who want to expand their portfolios without relying on traditional income verification.

Ridge Street Capital works with real estate investors nationwide to:

- Approve deals with low or borderline DSCR

- Finance STR and LTR properties

- Offer competitive rates with fast closings

- Help structure deals to meet DSCR guidelines

- Provide bank-statement, no-income, and LLC-friendly lending

Learn more about Ridge Street’s DSCR loan programs.

Requirements for a DSCR Loan FAQs

What minimum DSCR do lenders typically require?

Most lenders require between 1.0 and 1.25, meaning the property must generate at least enough income to cover its mortgage payments.

Can I qualify with lower credit?

Some lenders accept scores down to 620, though higher credit often improves terms. Ridge Street Capital requires a minimum credit score of 660+.

Do DSCR loans require personal income proof?

No. Approval is based on rental income and property cash flow, not tax returns or pay stubs.

Can I use a DSCR loan for short-term rentals?

Yes, specialty DSCR lenders will allow Airbnb or vacation rental income if supported by the AirDNA projected cashflow or strong short-term rental history.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)