Top 5 Investment Property Lenders in 2026

February 27, 2026

Finding the right lender for an investment property can determine whether your deal closes on time or falls apart entirely. Unlike primary residence conventional mortgages, investment property loans require specialized underwriting that accounts for rental income, property cash flow, and investor experience, not just your W-2 or bank statement. That means the lenders who serve investors well are not the same institutions that serve personal homebuyers well.

Investment property loans are a broad financing category that covers three distinct strategies: rental loans (typically DSCR) for buy-and-hold and portfolio investors, Fix & Flip loans for acquisition and renovation, and construction loans for ground-up builds. Each operates on different underwriting logic, pricing, and timelines.

This guide evaluates the best lenders across all three investment property loan types – if you are specifically focused on DSCR rental financing, see our dedicated Best DSCR Lenders guide for a deeper comparison of rental loan programs specifically.

Who Are the Best Investment Property Lenders in 2026?

Below are the top investment property lenders for 1-4 unit rentals, fix-and-flip projects, short-term rentals, and rental property portfolios.

This list was created by considering the competitiveness of loan terms, lowest rates, low fees, closing times, and regional coverage of U.S. based investment property lenders.

Terms and requirements vary by market and borrower profile. Always confirm current terms directly with the lender. Table values reflect common investor baselines, not guaranteed terms.

Comparing the Best Lenders for Investment Property

The goal of these lender review summaries is to help real estate investors compare loan options and lender options based on product variety, requirements, rates, and terms.

The types of loan product compared and review are outlined below:

Types of Investment Property Loans Included In This Review

Investment property lenders specialize in loan products that conventional banks and residential mortgage companies typically do not offer. This guide focuses on the 3 most common investment property loan products: DSCR Loans, Fix & Flip Loans, and Construction Loans.

- DSCR Loans: 30-year loans designed for rental properties which are underwritten using property’s rental income rather than the borrower’s personal income.

- Hard Money / Fix & Flip Loans: Short-term interest-only loans designed to allow investors to purchase distressed properties by providing financing for the acquisition and rehab of the property. Fix and flip loans are underwritten based on the after-repair value (ARV) of the property which allows investors to access higher leverage.

- Ground-Up Construction Loans: Draw-based financing for new builds. Loan proceeds are reimbursed to builders as development gets completed in “draws”.

Below is Ridge Street’s detailed lender breakdown, structured around the factors that matter most to real estate investors.

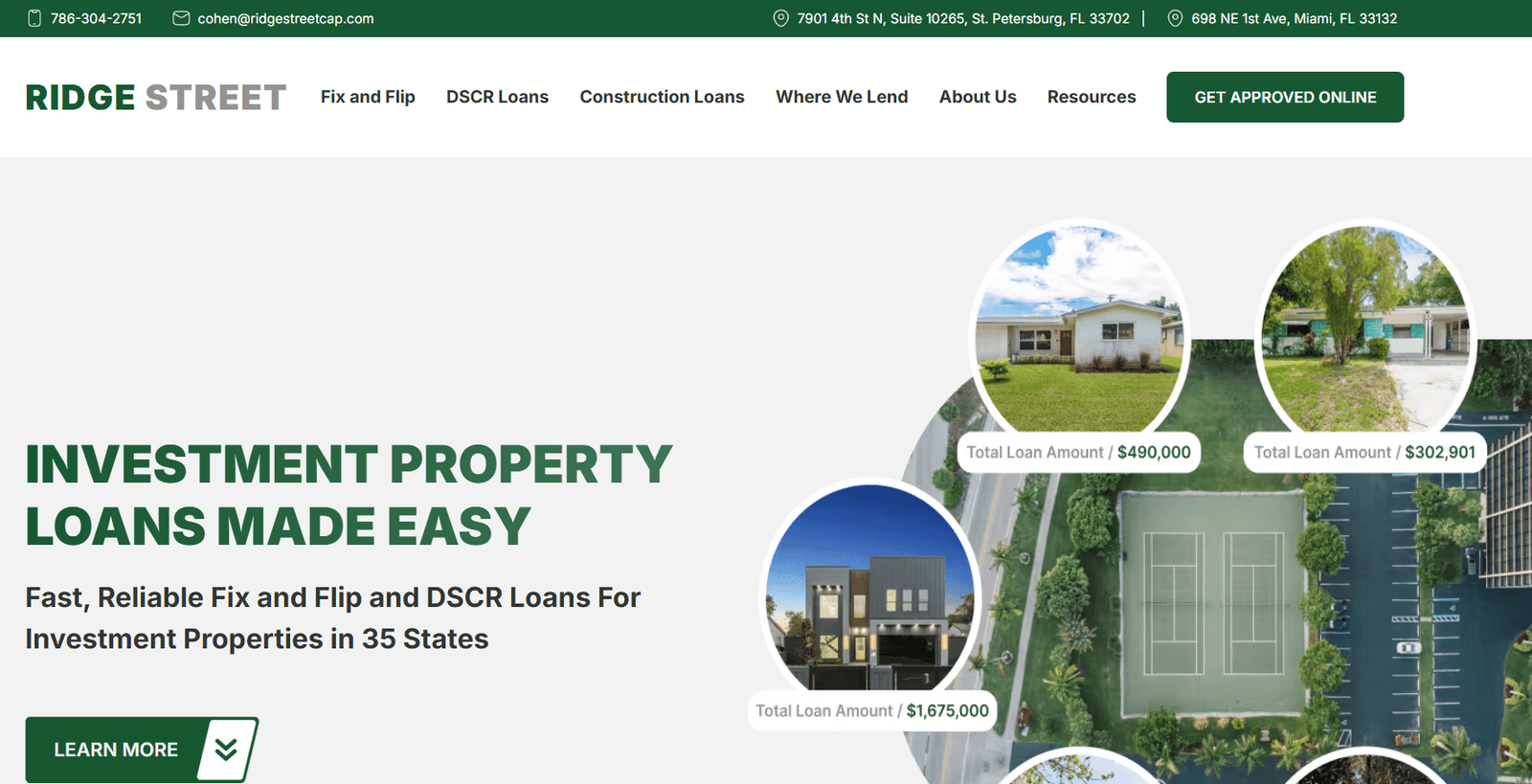

1. Ridge Street Capital (Editor’s Pick – Best Overall for Active Investors)

Overview:

Ridge Street Capital is a private real estate lender built specifically for real estate investors who want speed, flexibility, and scalable financing — without the bureaucracy of traditional banks.

Based in Miami and lending in 35 states, Ridge Street focuses exclusively on investment property loans. Unlike generalist lenders, every program is designed around the needs of fix-and-flip operators, BRRRR investors, and rental portfolio builders.

What separates Ridge Street from most lenders is its investor-first structure: highly competitive DSCR rates (including a short-term rental DSCR program), beginner-friendly fix-and-flip terms, and industry low fee structures, including 0% origination options on DSCR loans.

The loan application process is streamlined and term sheets are typically issued within 2 business hours. Fix & Flip loans close in 7–10 days, while DSCR loans close in 21-25 days — consistently faster than most rental lenders.

Key Programs:

- DSCR Loans (Long-Term Rentals & Airbnb Loans)

- Fix & Flip Loans (Acquisition + Renovation)

- BRRRR Strategy Financing (Hard Money + Cash Out Refinance DSCR Loans)

Best For:

- BRRRR investors scaling rental portfolios

- Short-term rental (Airbnb) investors seeking competitive DSCR options

- First-time Fix & Flip investors who need guidance

- Investors prioritizing low fees and fast closings

Pros and Cons:

Pros:

- Extremely competitive STR DSCR program

0% origination option on DSCR loans - Term sheet in ~2 business hours

- 7–10 day Fix & Flip closings

- 21-25 day DSCR closings (faster than most rental lenders)

- Beginner-friendly Fix & Flip program

- Works with smaller loan sizes

- Streamlined online application process

Cons:

- Limited to 35 states (not nationwide)

- Loan caps: $3M (Fix & Flip) and $2M (DSCR)

- Not designed for large commercial/multifamily syndications

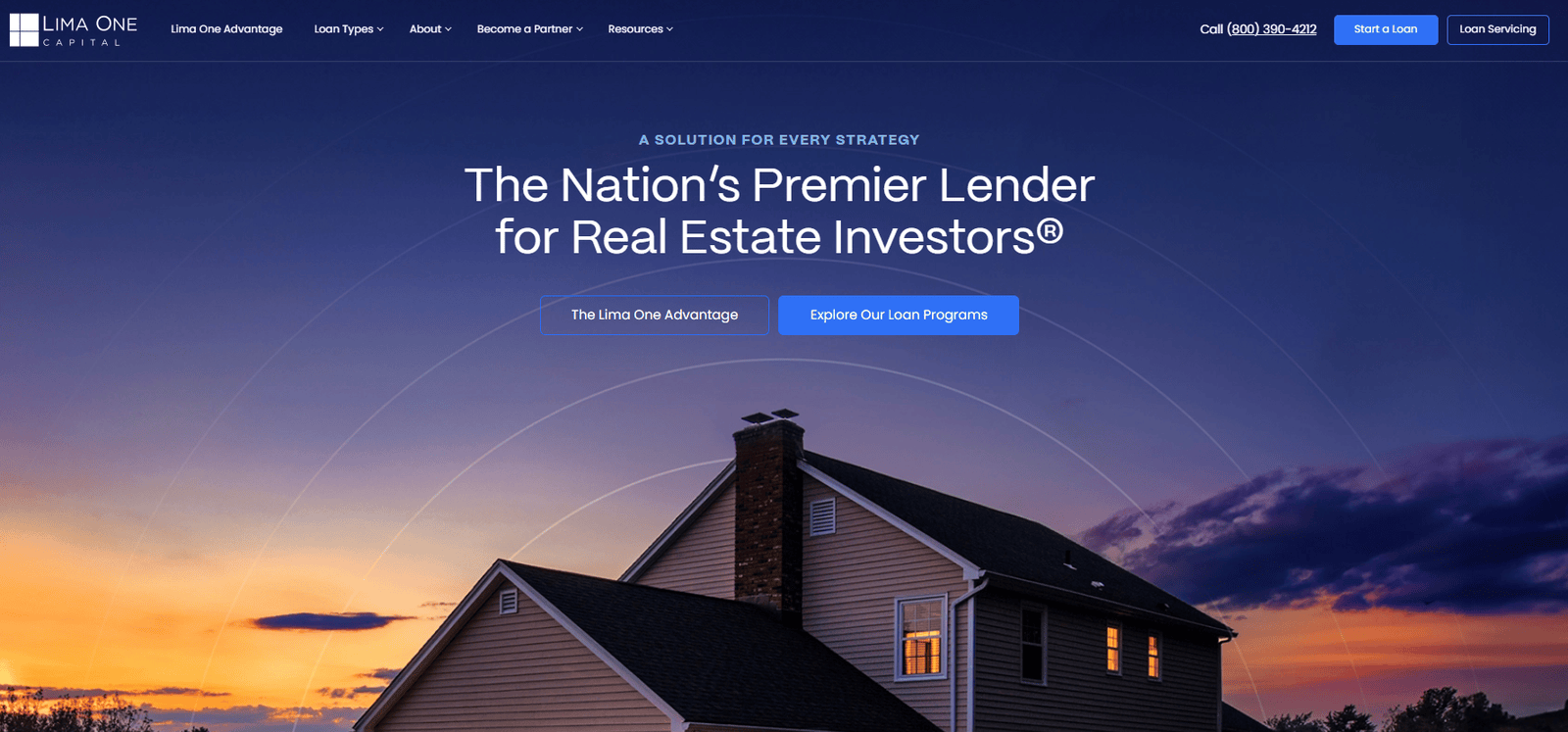

2. Lima One Capital

Overview:

Lima One Capital is a national private lender based in Greenville, South Carolina, with over $2 billion in funded real estate investor loans. Their product range covers Fix & Flip, DSCR rentals, portfolio loans, ground-up construction, and bridge financing. The in-house servicing model manages the full loan lifecycle from origination through draw funding, reducing third-party delays on renovation projects.

Lima One is particularly strong for investors managing growing portfolios, including those consolidating multiple properties into a single blanket loan or refinancing into a portfolio DSCR structure.

Key Programs: Fix & Flip, DSCR Rental, New Construction.

Qualification: 660 minimum FICO (Fix & Flip & DSCR). Fix & Flip: 7.5% down. DSCR: 20% down.

Best For: Investors managing 5 or more properties, BRRRR operators who want portfolio refinance options in one place, and multifamily or new construction developers.

Pros and Cons:

Pros:

- Self-serve term sheet tool generates pricing without a sales call.

- 90% LTC on construction (among the highest available from any national lender).

- Higher loan limit on Fix & Flip loans with up to $5M property value.

Cons:

- Longer closing speed for loan underwriting.

- Underwriting tends to favor experienced investors — newer borrowers often report more friction and tighter conditions.

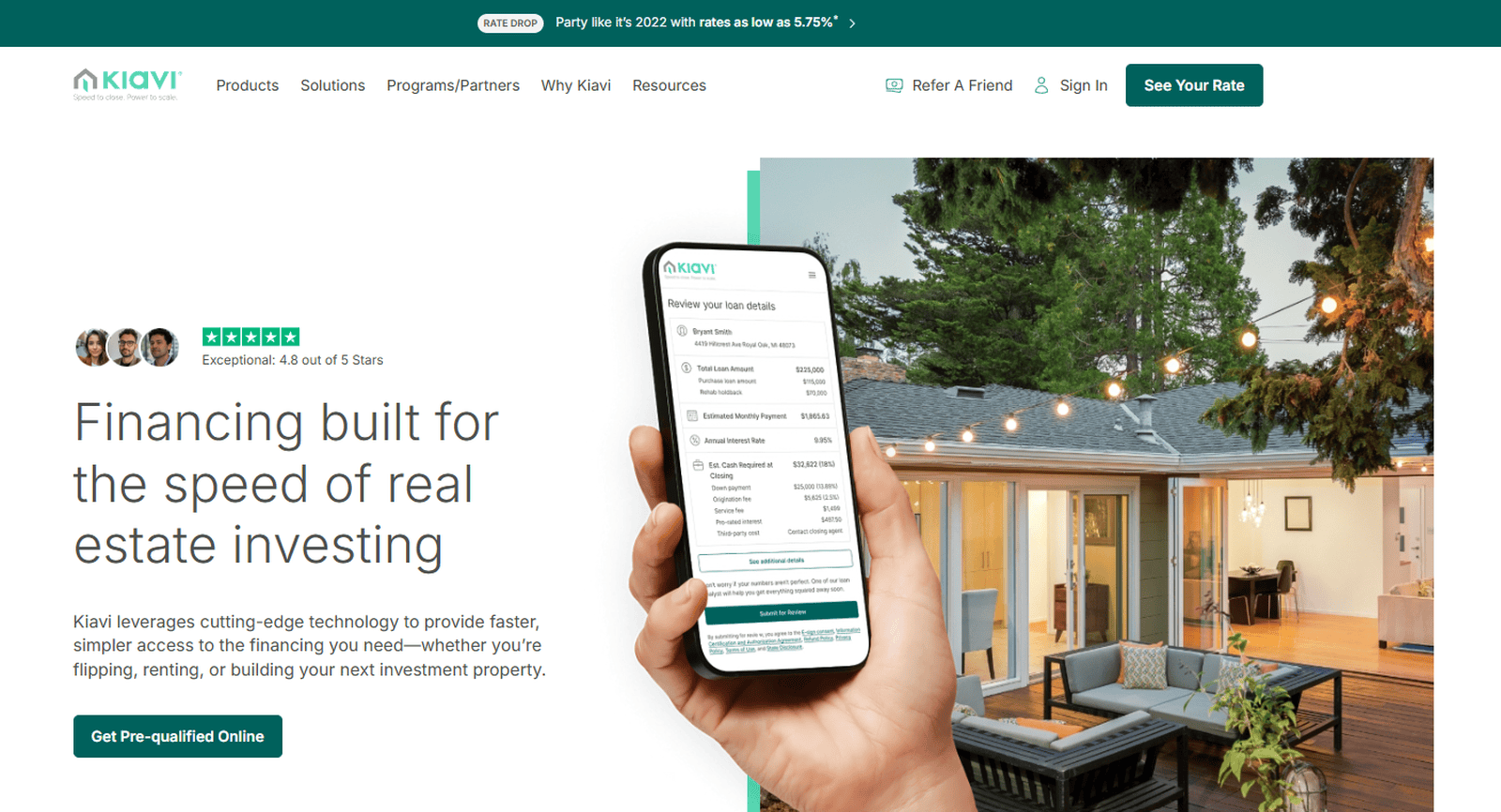

3. Kiavi

Overview:

Kiavi is a nationwide private real estate lender that uses a tech-driven platform to finance investors flipping, renting, or building residential investment properties, including single-family rentals and small portfolios.

Their platform uses machine learning, automated underwriting, and real-time data pricing to close faster than most manually underwritten lenders. The fully digital process makes Kiavi especially well-suited for experienced investors running multiple deals simultaneously.

Key Programs: Fix & Flip, DSCR Rental, New Construction

Qualification: 640 minimum FICO. Fix & Flip: 5% down. DSCR: 20% down. Min DSCR 1.1 to pre-qualify for rental loans.

Best For: Experienced, high-volume investors who prioritize speed and automation over relationship-based service, and tech-forward operators scaling across multiple markets simultaneously.

Pros and Cons:

Pros:

- Fully digital application — online pricing with no sales call required.

- Fix & flip closings within 10 days

- No prepayment penalties on Bridge and Fix & Flip loans.

Cons:

- DSCR of 1.1, stricter than most lenders.

- Platform-driven process with less flexibility and stricter documentation requirements

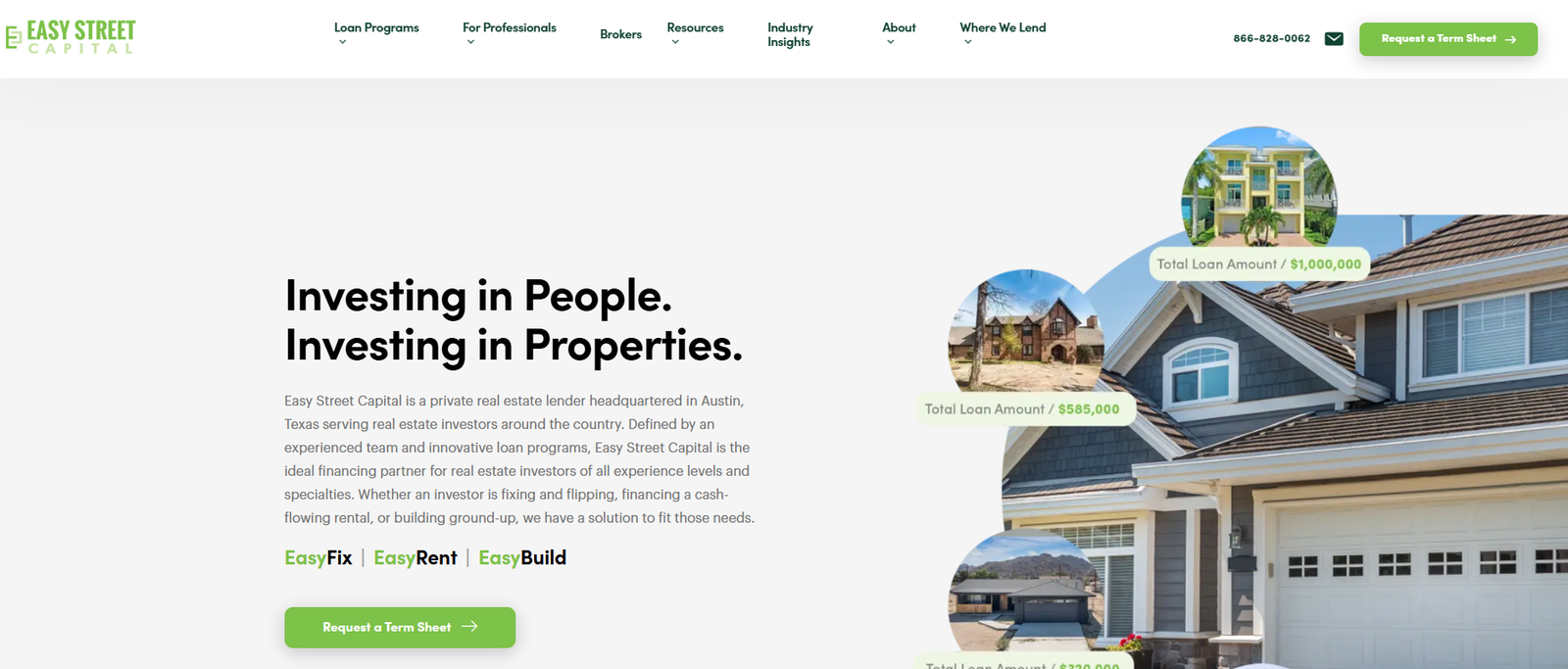

4. Easy Street Capital

Overview:

Easy Street Capital is a private lender based in Austin, Texas, built around transparency. Investors can generate their own term sheets online before speaking to a loan officer, which makes deal feasibility analysis faster and removes the usual back-and-forth from early-stage conversations.

Positioned as a flexible and competitive terms lender, Easy Street Capital offers solutions for anyone – from first-time investors dipping into industry veterans looking to rapidly expand their portfolios. The minimum FICO score of 600 for Fix & Flip loans is lower than most private lenders, making Easy Street one of the more accessible options for investors earlier in their career.

Key Programs: EasyFix (Fix & Flip), EasyRent (DSCR Rental), EasyBuild (New Construction)

Qualification: 600 minimum FICO (Fix & Flip), 640 (DSCR), 680 (construction). Fix & Flip: 10% down, DSCR: 20% down payment.

Best For: Fix & Flip investors who need to close fast or have deals other lenders won't touch. DSCR investors with sub 1.0 DSCR ratio properties or credit scores below 640.

Pros and Cons:

Pros:

- Operates in 48 states.

- Low credit score floor.

- Closing on Fix & Flip loans within 7 business days.

Cons:

- Higher rates and fees.

- The underwriting process can require additional documentation close to closing.

5. Griffin Funding

Overview:

Griffin Funding is a direct-to-consumer non-QM lender operating in all 50 states with a product line built specifically for borrowers who don't fit conventional mortgage guidelines. Where most private lenders stop at DSCR, Griffin extends into the full range of non-QM financing: bank statement loans for self-employed investors, asset-based loans for high-net-worth borrowers, 1099 and P&L loans for contractors and business owners, and VA loans for veterans. That range makes Griffin the rare lender that can finance both the investment property and the borrower's conventional mortgage under one roof.

Key Programs: DSCR Rental, Fix & Flip, Bank Statement, VA, Conventional, HELOC.

Qualification: 620 minimum FICO (580 for VA). DSCR: 20% down. Fix & Flip: 20–30% down.

Best For: Self-employed investors, veterans and personal mortgage products under one lender. Particularly strong for investors whose taxable income understates actual cash flow.

Pros and Cons:

Pros:

- Operates in all 50 states.

- Broad non-QM product menu.

- Loans up to $20M.

Cons:

- Rates tend to be relatively higher than those of dedicated private lenders.

- Closing timelines are relatively longer than most lenders in this guide.

How to Choose the Right Investment Property Lender

The right lender depends on your strategy, your deal timeline, and your loan type. The two most commonly used products in investment property financing — DSCR loans and hard money — serve fundamentally different purposes. DSCR loans are long-term, income-based, and designed for stabilized rentals (long-term rentals and short-term rentals). Hard money / Fix & Flip loans are short, deal-based, and designed for acquisitions and renovations. Many strategies, including BRRRR, use both in sequence.

The table below maps investor profiles to the right lender and loan type.

Before committing to any lender:

- Confirm the loan type matches your real estate investment strategy and property condition.

- Get the term sheet in writing and review origination fees, prepayment penalties, and reserve requirements alongside the rate.

- Ask specifically about closing timelines and what can delay them.

- Stress-test your DSCR at a rate 0.5%-1% higher than quoted. If rates move before you close, you need to know the deal still works.

Investors building in specific regions often benefit from regional specialists. For example, a Florida hard money lender may offer better terms for Miami deals than a national platform, while Texas DSCR loans come with state-specific nuances worth understanding.

Ready to Apply? 5 Steps to Qualify for an Investment Property Loan

Investment property loans have different qualification standards than residential mortgages. Here is what most private and DSCR lenders look for:

1. Know your credit score. Most investor-focused lenders set a floor of 660, but your score also determines your rate tier. Pull your credit before picking a lender so you know which programs you can access and where there is room to improve terms.

2. Confirm your down payment source. Lenders will ask where your down payment is coming from and how long it has been in your account. Make sure your funds are seasoned and documented before you get to underwriting — last-minute transfers raise flags.

3. Check your property condition. If the property needs significant work, it needs a hard money loan — DSCR lenders require properties to be move-in ready and income-producing. Trying to force a distressed property into a DSCR program is a common application mistake investors make.

4. Have a defined exit before you close. For Fix & Flip and bridge loans, lenders want to know how you are getting out — sale or refinance. If you're pursuing a BRRRR method project, get pre-approved with a DSCR lender before you close the hard money loan. That single step eliminates the most common BRRRR failure point of not being able to refinance out of your hard money loan.

5. Get your loan terms in writing. Before paying any upfront fees or authorizing an appraisal, get the full term sheet in writing.

If you are ready to run the numbers on your next deal, Ridge Street Capital issues term sheets within 2 business hours and offers pre-approval letters to investors with properties lined up.

Best Investment Property Lenders FAQs

How do investment property loans differ from residential mortgages?

Investment property loans are underwritten on different criteria than residential mortgages. Where a residential lender evaluates your personal income, employment history, and debt-to-income ratio, investment property lenders focus on the asset — the property's cash flow, after-repair value, or rental income potential. That shift in underwriting logic is what makes these loans accessible to self-employed investors, LLC borrowers, and portfolio builders. In most cases, the qualification process is faster, documentation requirements are easier, and the decision is driven by deal economics rather than personal financial history.

How much cash should you have in reserves for an investment property loan?

Most lenders require cash reserves equal to six months of mortgage payments for an investment property loan. These reserves help cover monthly mortgage payments, insurance, taxes, and other loan costs if rental income is interrupted

Can investment property loans have interest-only payments or flexible terms?

Yes. Investment property loans are generally more flexible in structure than residential mortgages. Fix and flip loans are typically interest-only for the full loan term, keeping monthly payments low during the renovation period.

Many DSCR loans also have interest-only options, usually for the first 5 to 10 years, before converting to a fully amortizing payment. Eligibility depends on factors such as property type, loan amount, credit score, and rental income. For investors, interest-only structures help preserve cash flow during stabilization or renovation periods.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)