Fix and Flip Loans Explained: The Complete Fix and Flip Financing Guide (2026)

January 31, 2026

Traditional mortgages and conventional loans rarely work for properties that need renovation because banks will not finance heavy repairs. Fix and flip loans fill that gap by offering short-term financing that lets real estate investors purchase and renovate distressed properties quickly and resell them for profit.

Fix and flip loans are designed to cover both the property purchase and the rehab budget, so investors can acquire distressed properties with as little as 10% down.

This guide explains how fix and flip loans work, how lenders evaluate fix and flip projects, fix and flip loan program options, the costs to expect, and common mistakes to avoid when exploring fix and flip financing.

What Is a Fix and Flip Loan?

A fix and flip loan is an asset-based short-term financing option provided by non-bank private lenders designed for real estate investors to buy properties and complete renovations within a 6-12 month window before reselling for a profit.

Fix and flip loans carry a term of 6-18 months, with most fix and flip loan programs offering a 12-month term. These loans cover both a portion of the purchase price and the renovation budget in one package. This means that investors can buy distressed real estate with as little as 10% down plus closings and have the funding to complete the rehab of the property.

Most fix and flip loans have an interest-only rate structure, meaning monthly payments only include interest and not principal. This keeps the monthly interest payment lower than amortizing loans, allowing investors to stay liquid while completing their projects.

When the properties are finished and sold, the fix and flip loan is repaid through a balloon payment where the entire principal balance is paid back using the proceeds from the sale.

How Do Fix and Flip Loans Work?

Fix and flip financing is structured around the profitability of the flip project, not the borrower’s W-2 income. Instead of focusing on tax returns or personal debt-to-income ratios, fix and flip lenders evaluate whether a property can realistically be purchased, renovated, and resold at a profit.

Loan Structure: Initial Advance and Rehab Holdback

A typical fix and flip loan is split into two components:

- Initial Advance: This portion of the loan is disbursed at closing to secure the property, usually covering 80–90% of the purchase price.

- Rehab Holdback: Funds designated for renovations are released in stages (called “draws”) as renovations are completed. Many fix and flip loans cover up to 100% of rehab costs, as long as the total loan remains below 75% of the ARV.

Dutch vs Non-Dutch Interest

Interest payments are determined in one of two ways: Dutch Interest and Non-Dutch Interest:

- Dutch Interest: Interest is calculated on the full loan amount, including unreleased rehab funds, from day one. This means even if the lender hasn’t yet disbursed all of the rehab budget, the interest accrues on the entire approved loan balance.

- Non-Dutch Interest: Interest is only charged on the funds that have actually been disbursed. For example, if a portion of the rehab holdback hasn’t been released yet, no interest accrues on those unreleased funds.

Why it matters: Choosing between Dutch and non-Dutch interest affects carrying costs and cash flow during the project.

- Dutch interest loans result in slightly higher interest carrying cost since the full loan accrues interest from day one.

- Non-Dutch interest loans allow investors to save on interest while rehab funds are in escrow, reducing the loan carrying costs of the project.

How Lenders Assess Deals

After a real estate investor identifies a potential fix and flip opportunity, lenders evaluate both the property and the borrower to determine the fix and flip loan terms that can be offered.

Several key factors influence the loan amount, structure, and terms:

- Scope of the Rehab:

Lighter cosmetic renovations are lower risk and typically allow higher leverage. Larger, structural, or complex rehabs are riskier and may receive more conservative financing terms. - Projected Profit Margin:

Deals with higher potential returns and lower LTARV are considered lower risk and qualify for higher leverage. Investors should target a minimum profit margin of 30% (Return On Cash) to qualify for max leverage. - Borrower Experience:

Investors with a track record of successful flips often qualify for higher leverage, especially on heavier or more complex renovation projects.

Note: Ridge Street offers a High Leverage Program for first-time investors with strong credit that allows beginner flippers to obtain 90% of Purchase + 100% of Rehab on their first project. - Creditworthiness:

While fix and flip loans are primarily asset-based, a strong FICO score signals reliability and improves the fix and flip loan’s interest rate and maximum loan-to-value ratio.

You can use our fix and flip loan calculator to check the projected profit of your project with fix and flip financing.

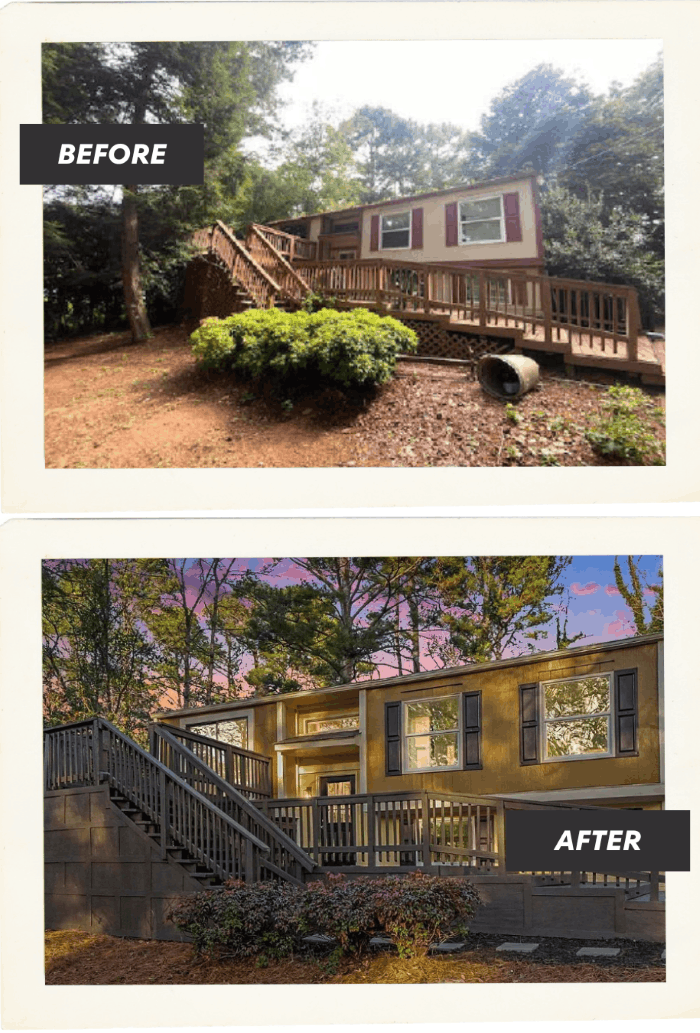

Funded Fix and Flip Loan Example

The example provided below is a fix and flip loan in Georgia (Atlanta area) that Ridge Street Capital provided to a first-time house flipper.

The fix and flip loan covered 80% of the $180,000 purchase price and 100% of the $60,000 rehab budget. The interest rate was 10.99% for 12 months and Ridge Street charged a 2.5% origination fee.

The property was completed and sold in 6 months for $342,000 after being listed on the market for less than 24 hours.

After closing costs and loan carrying costs, the borrower turned a $54,000 profit within 6 months producing over a 100% cash-on-cash return.

Ridge Street’s Fix and Flip Loan Program Details

Ridge Street has three designated fix and flip loan programs categorized by investor experience, ranging from a Beginner Program to an Expert Program.

Ridge Street’s Beginner Fix and Flip Loan Program

This fix and flip program is designed specifically for first-time fix and flip investors.

*Notes:

- This beginner fix and flip program is not available in flagged markets including: Philadelphia, Baltimore, and Cleveland.

- Non-Dutch interest available for all loans over $100,000.

Ridge Street’s Intermediate Fix and Flip Loan Program

This fix and flip program is designed specifically for intermediate real estate investors with one to 3 fix and flip projects completed within the last 5 years.

*Note:

- This intermediate fix and flip program is subject to a 5% leverage reduction in flagged markets including: Philadelphia, Baltimore, and Cleveland.

- Non-Dutch interest available for all loans over $100,000.

Ridge Street’s Expert Fix and Flip Loan Program

This fix and flip program is designed specifically for intermediate real estate investors with five or more fix and flip projects completed within the last 5 years.

*Note:

- This expert fix and flip program is subject to a 5% leverage reduction in flagged markets including: Philadelphia, Baltimore, and Cleveland.

- Non-Dutch interest available for all loans over $100,000.

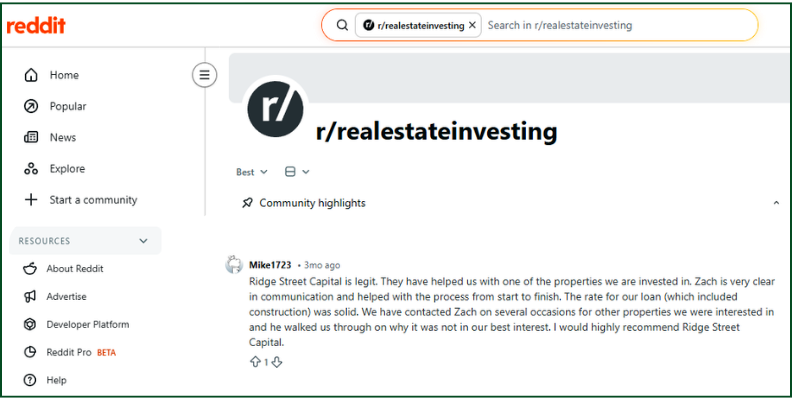

Case Study: Fix and Flip funding — Denver, Colorado

Case numbers:

The borrower was a first-time fix and flip investor acquiring a property in Denver at $260,000. Ridge Street funded 90% of the purchase and 100% of the $54,100 renovation budget in a single loan. The rehab budget was submitted virtually with photo documentation across all renovation categories — demolition, exterior, interior, MEP, appliances, and site work. At a $400,000 ARV, the loan closed at 72% ARLTV within 9 days. The client proceeded with the flipping project and left a comment on Reddit:

Before committing capital to a project, it's worth asking is it profitable to flip houses in the current market.

Fix and Flip Loan Process Breakdown

Experienced fix and flip lenders can close on financing quickly. Many “investor deals” are sourced off-market or through wholesalers who are often required to close quickly. Fix and flip loans can close in as little as 7 days with average closing times around 10 days.

Below is a detailed breakdown of the fix and flip loan process:

1. Deal Submission or Pre-Approval (5 mins)

Investors submit a brief application with details about the property, renovation plan, experience, and credit profile. Investors who don’t have a property lined up yet can submit a pre-approval application to make sure they qualify as a borrower.

2. Term Sheet or Preliminary Offer (2 hours)

A Term Sheet outlining the proposed loan is issued, including: loan amount, LTC, rehab funding, rate, costs, and estimated cash to close. This gives the investor a clear preview of loan structure before moving forward.

3. Document Submission (1 day)

Once the borrower has the property under contract, they provide ID, entity documents, the purchase contract, Scope of Work (aka Rehab Budget), and bank statement showing cash to close.

4. Appraisal and Property Evaluation (5-7 days)

A licensed appraiser is then sent to inspect the property. An as-is value and an after-repair value is included in the report. Lenders use these values to confirm LTV calculations.

5. Final Underwriting (24 hours)

Once the appraisal is complete, the loan is formally underwritten. In this stage, the loan is simply being “double checked” to make sure all documents are collected and the appraised values came in on target.

6. Closing and Funding (48 hours)

Once underwriting and appraisal are complete, closing is scheduled within 48 hours. Funds are wired the same day, allowing investors to start their projects quickly.

Costs and Fees Associated with Fix and Flip Loans

Fix and flip loans have higher costs than most traditional mortgage products, including both higher closing costs and interest rates.

Below is a breakdown of all of the costs associated with a fix and flip loan:

- Origination Fees: Fix and flip lenders charge 1% - 4% of the total loan amount as an origination fee. For example, a 2% origination fee (also called 2 points) on a $200,000 loan equals $4,000. Borrowers with strong credit and experience qualify for lower origination fee structures.

- Legal/Processing/Underwriting Fee: Most lenders will charge a $1,250-$1,995 Underwriting Fee (also called a “processing fee” or “legal fee”) to cover their operational costs of closing a loan (credit check, background check, legal drafting of the mortgage package, etc)

- Interest Payments: As with any loan, borrowers will pay interest on the funds being borrowed. Most fix and flip loans have an interest rate of 10%-13% with a variation of dutch and non-dutch interest rate options being available.

- Non-Lender Costs: With any real estate transaction, buyers incur “non-lender” costs. These include:

- Title Insurance: Title insurance is an insurance policy that is used by the title company to make sure that the transfer of ownership from seller to buyer is done correctly and insured in case of an error. Typical title insurance policies range from $1,000-$3,000 depending on the dollar amount being insured.

- Hazard/ Builder’s Risk Insurance: House flippers are required to obtain insurance for the construction they’re doing on the house. Depending on the market the property is located in and the dollar amount of the insurance policy, costs can range from $1,500-$2,000 in most real estate markets for house flipping like (Atlanta, Indianapolis, Dallas, etc.) to $5,000-$10,000 in the most expensive insurance markets (Miami, Tampa / St. Petersburg, etc).

- County/State Fees: Most U.S. Counties charge a small fee of $200-$500 for recording the mortgage in the county public records. Some regions will impose an additional “mortgage tax” or “land transfer tax” in the range of 1%-2% of the property value. Some regions where these mortgage tax / transfer taxes apply are New York, Florida, Massachusetts, and Pennsylvania.

- Draw Fees: Fix and flip lenders typically charge between $200-$300 per rehab draw.

In total, an average fix and flip project has closing costs between 3% to 6% depending on the lender, property location, and non-lender costs.

Common Fix and Flip Loan Mistakes to Avoid

Even experienced investors run into problems when they move too fast or underestimate project risks. Here are the most common mistakes house flippers make and how to avoid them.

1. Overestimating ARV

The fastest way to lose money on a flip is assuming the property will sell for more than the market supports. Always use sold comps (not active listings) and verify that the planned renovations match the neighborhood.

2. Underestimating Renovation Costs

Contractor bids that look too low usually are. Add a buffer of 5 to 10 percent for rehab scope changes, unexpected repairs, and delays. Cost overruns are one of the top reasons house flippers lose money on their projects.

3. Ignoring Holding Costs

Interest payments, taxes, insurance, utilities, and maintenance add up quickly. A six-month project can cost thousands in carrying costs. Real estate investors should have cash reserves for at least 6 months of holding to ensure they don’t run out of cash while completing the project.

4. Hiring the Cheapest Contractor

Cheap bids lead to poor work, missed deadlines, and blown budgets. Work with contractors who specialize in investment renovations and have verifiable results.

5. Not Having a Backup Exit Strategy

If the house market slows, you don’t want to get stuck with your house on the market for 6 months. Before closing on your fix and flip, check to see if you will be able to refinance out of your fix and flip loan with a DSCR loan based on the expected after-repair value and market rent.

Note: You can check the refinance exit strategy for your fix and flip project with our DSCR Loan Calculator.

6. Overleveraging in Weak Markets

High-crime areas, rural locations, or neighborhoods with declining demand require conservative offers and lower LTV ratios. It is very common for investors who invest in their local markets not to regularly review the number of homes listed vs the number of homes sold in their area. Making sure that the market you're investing in has regular and consistent sales volume is paramount for consistent fix and flip success.

Alternative Fix and Flip Financing Options

Business Lines of Credit

A business line of credit provides a revolving credit limit that real estate investors can use to fund multiple projects at once. Investors draw only what they need, and interest accrues only on the borrowed amount.

That said, business lines of credit are not real estate loans (i.e. mortgages), instead they are secured by the business themselves. Borrowing entities typically need 12-24 months of business financials showing annualized revenue of at least $100K-$250K, with enough profit to cover the debt-service of the business loan.

This financing option is only ideal for real estate investors who have other cash-flowing businesses to use as collateral. A business line of credit is not a viable option for most first fix and flip investors.

Home Equity Line Of Credit

A home equity line of credit allows investors to use equity from their primary residence to fund projects, often at lower rates than other house flipping financing sources. Borrowing capacity can be as high as 75 to 85 percent of the home’s value.

Approval and funding can take several weeks, so this option fits planned acquisitions rather than urgent opportunities. Investors should consider the added risk of using their personal residences as collateral, especially during market downturns.

Personal Line Of Credit

Personal loans offer smaller limits, generally up to $100,000, and require the borrowers to have high W-2 income. The personal lines are often offered by banks and smaller fintech-lenders and are based on the borrower’s personal income. This option is usually best for real estate investors who have regular jobs and are pursuing smaller flip projects on the side. Personal lines of credit typically have higher interest rates than most fix and flip loan options so borrowers should be cautious about the higher carrying costs of personal loans.

Getting a Fix and Flip Loan

If you’re serious about pursuing a fix and flip project, the next step is understanding the loan terms you may qualify for before you make an offer. Most experienced investors do this early so they can move quickly when the right deal appears.

At Ridge Street Capital, the process is straightforward:

- Submit basic property and borrower details through our Quick Application.

- Answer 2-3 additional questions about the property or your profile via email.

- Receive a Term Sheet and Pre-Approval Letter within 2 business hours.

Having formal terms in hand allows you to analyze deals with real numbers—not assumptions.

Fix and Flip Loans FAQs

What’s the difference between LTV, LTC, ARV, and LTARV?

- LTV measures leverage against the property’s current value.

- LTC measures leverage against the total project cost (purchase + rehab).

- ARV is the property’s projected value after renovations.

- LTARV measures leverage against the property’s after-repair value.

- Lenders use all four to size and determine the total loan amount for your fix and flip loan.

Can I finance 100 percent of a fix and flip project?

Most lenders require 10–20 percent down on the purchase, but many will finance up to 100 percent of the renovation budget. Full financing is rare because lenders want investors to have some cash in the deal to reduce risk.

What is the 70% Rule in Real Estate?

The 70% rule is a quick deal-analysis guideline investors use to estimate their maximum purchase price on a fix-and-flip. It suggests an investor should pay no more than 70% of a property’s after-repair value (ARV), minus renovation and holding costs.

The goal is to preserve a 20–30% profit margin to account for rehab overruns, selling costs, financing fees, and market risk. Investors often adjust the percentage based on market conditions—closer to 75% in strong markets and as low as 65% in softer ones.

Importantly, the 70% rule is not a lender requirement. It’s an investor underwriting tool. Fix-and-flip lenders typically base loan amounts on loan-to-ARV (LTARV), often up to 75% for qualified borrowers.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)