DSCR Loan Pre-Approval: What It Is and How to Get One

May 14, 2026

A DSCR loan pre-approval is a conditional commitment from a lender to finance up to a specified loan amount based on the borrower's profile and the projected deal structure. No tax returns, W-2s, or personal income verification are required. The pre-approval letter confirms to sellers that the buyer's financing has been reviewed by a lender. This article explains the difference between pre-qualification and pre-approval, what the process requires, and how a DSCR pre-approval letter works in practice.

DSCR Pre-Qualification vs. Pre-Approval: What Is the Difference?

When buying real estate, sellers give preference to buyers whose financing is verified rather than estimated. Obtaining a lender letter, whether pre-qualification or pre-approval, signals serious intent to sellers and reduces the risk of the deal falling through at the financing stage. Which letter to pursue depends on where the investor is in the process.

What DSCR Pre-Qualification Gives You

Pre-qualification at Ridge Street Capital typically takes the form of an initial call or email exchange. The investor describes the deal profile, and the lending team assesses whether it makes sense. Investors submit no documents, and no credit check runs at this stage. Typically, investors use pre-qualification to confirm basic eligibility before preparing a formal application or while still in the early stages of the property search.

Pre-qualification provides a directional assessment, not a lender commitment. Sellers and listing agents generally understand this distinction, which is why a pre-qualification letter carries limited weight in a competitive offer situation.

DSCR Loan Pre-qualification: at a glance

- Informal, usually an email or short letter

- No documents, no credit pull, no formal letter

- Useful for confirming early eligibility

- Limited weight with sellers

What DSCR Pre-Approval Gives You

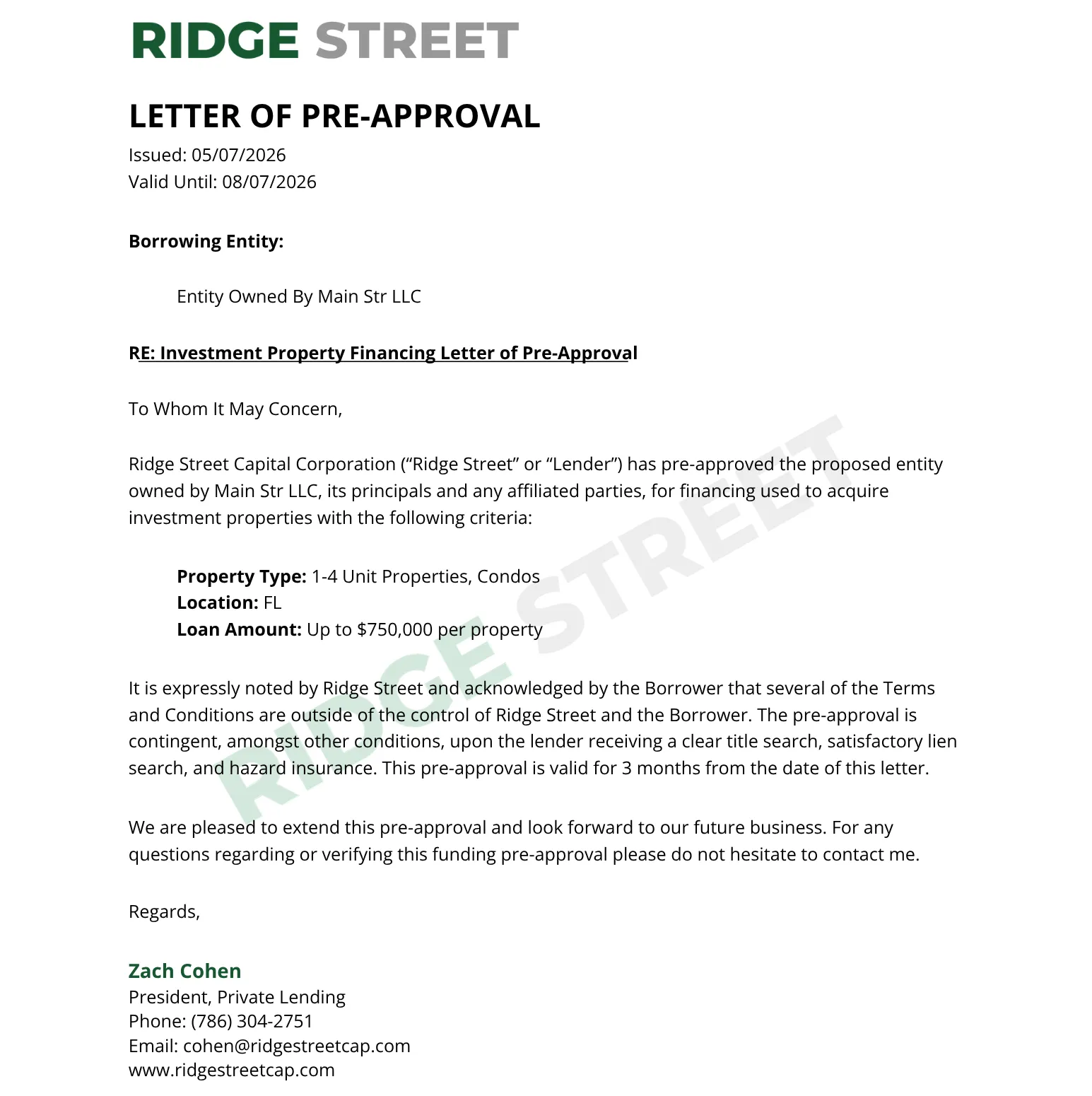

Pre-approval is a conditional commitment to finance a specific loan amount, issued after the lender has reviewed the borrower's documents and deal profile. DSCR pre-approval works differently from a conventional mortgage pre-approval. A conventional pre-approval evaluates personal income, debt-to-income (DTI), and credit score, and returns a general mortgage ceiling. A DSCR pre-approval is more specific. For a full comparison between the two financing structures, see the DSCR vs. conventional loan guide.

Before issuing the letter, a Ridge Street Capital loan officer asks about the property type, investment strategy, target location, and deal status. Ridge Street Capital issues the letter for a specific property type rather than an open-ended borrowing estimate, which makes it a more accurate and credible document.

DSCR Loan Pre-approval: at a glance

- Documents and the deal profile are reviewed before the letter is issued

- Indicates a specific loan amount and property type

- Confirms to sellers that the buyer's financing has been checked by a DSCR lender

- Valid for 90 days; refreshable with updated documentation

DSCR Loan Pre-Qualification and Pre-Approval Compared

Documents and Information Required for DSCR Loan Pre-Approval

To issue a pre-approval letter, Ridge Street Capital asks the investor to provide the following:

- Property type and target state (or specific property address if available)

- Purchase price

- Market rents

- Estimated annual taxes and insurance

- Estimated liquidity covering the down payment and reserves

- Deal status: under contract, preparing to make an offer, or still searching

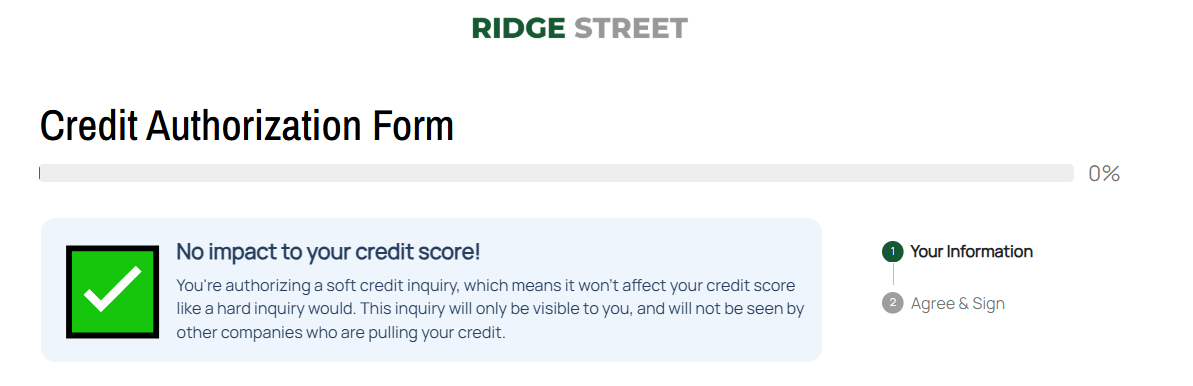

Once this information is provided, the lending team reviews the deal profile alongside a soft credit pull, a bank statement, and a government-issued ID. Investors who have not yet identified a property can start with a call. Ridge Street will review the numbers, discuss whether the deal structure makes sense, and confirm what financing terms the property may qualify for before issuing a pre-approval.

How Long Does DSCR Loan Pre-Approval Take?

The process runs in three steps and is completed the same day in most cases.

Step 1: Provide deal information and supporting documents. The investor shares the property profile details listed above along with a bank statement and ID. No full loan application is required.

Step 2: Receive a term sheet / pre-approval letter. If the investor has a specific property identified, a loan officer reviews the deal profile and issues a term sheet within 2 business hours, confirming the loan amount for that deal. If the investor has properties in consideration, Ridge Street issues a pre-approval letter in general terms covering the approved loan amount, eligible property type, and target state. At this stage, Ridge Street runs a soft credit pull. The letter is valid for 90 days from the date of issue.

Step 3: Full loan application on a specific property. Once the investor goes under contract on a property, the process moves into full underwriting. The loan application is submitted, the appraisal is ordered, and the pre-approval converts into a formal loan commitment based on the specific deal.

How a DSCR Pre-Approval Letter Strengthens Offers

A pre-approval letter from a private lender confirms to sellers that the buyer's financing has been reviewed against a specific deal profile. In practice, this produces four advantages for the investor.

Focused property search. The pre-approval confirms the loan amount and the property criteria the investor qualifies for. Investors enter the investment property search knowing exactly what the financing will support.

Stronger offers. Sellers evaluate financing reliability alongside the offer price. A letter backed by document review and a credit check carries more credibility than an unverified estimate.

Faster closing. Since the borrower's profile has already been reviewed, the underwriting is focused on the property, including the appraisal, title, and DSCR calculation. This generally speeds up the loan origination process.

Early identification of issues. Credit profile concerns identified early can usually be resolved before the deal is at risk. If the loan officer discovers the same issues during underwriting, this can delay or derail the transaction because the approaching deadline leaves fewer options to fix the problem.

For investors buying through an LLC, the pre-approval letter confirms the entity has been reviewed and the loan can close in that structure.

Get Pre-Approved for a DSCR Loan with Ridge Street Capital

Ridge Street Capital issues DSCR loan pre-approvals across 35 states for long-term rentals, short-term rentals, and multifamily properties. Term sheets are issued within 2 business hours. No income documentation required.

DSCR Loan Pre-Approval FAQs

Is DSCR loan pre-approval free?

Yes. Ridge Street Capital does not charge for the pre-approval or for the soft credit pull.

Does DSCR loan pre-approval require a hard credit pull?

No. Ridge Street Capital runs a soft credit pull at the pre-approval stage. A soft pull leaves the borrower's credit score unchanged and does not appear on the credit report. A hard pull may occur later, when the full loan application is submitted on a specific property under contract.

Can investors get pre-approved in an LLC name?

Yes. DSCR loans are business-purpose loans and commonly close in the name of an LLC. The pre-approval letter is issued to the borrowing entity directly. Investors closing in an LLC should have entity documents available: Articles of Organization, Operating Agreement, and EIN confirmation. For a full breakdown of how DSCR loans work under an LLC, see the DSCR loan for LLC guide.

What credit score is needed for DSCR loan pre-approval?

Ridge Street Capital requires a minimum of 660 FICO for long-term rental properties and 700 for short-term rentals and first-time investors. Credit score determines the rate and available leverage, not whether the property qualifies. For a full breakdown, see the DSCR loan requirements guide.

How long is a DSCR pre-approval letter valid?

Ridge Street Capital pre-approval letters are valid for 90 days from the date of issue. If the investor has not gone under contract within 90 days, Ridge Street refreshes the pre-approval with updated bank statements and a new credit review.

Does a pre-approval letter guarantee financing?

The pre-approval is a conditional commitment. It confirms the borrower's profile and deal parameters have been reviewed and approved for a specific loan amount, subject to satisfactory title search, lien search, and hazard insurance on the subject property. Final approval depends on whether the property meets the lender's requirements at appraisal and underwriting.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)