Rental Property Profit Calculator

July 1, 2026

Evaluating a rental property's profitability requires more than comparing rent to the mortgage payment. This Rental Property Profit Calculator applies vacancy, operating expenses, and debt service to calculate monthly cash flow, cap rate, cash-on-cash return, and debt service coverage ratio (DSCR). Results update automatically as you enter the property details.

How to Use the Rental Property Profit Calculator

Step 1: Enter the purchase details

- Enter the purchase price as the full contract price, not the appraised value.

- Set closing costs as a percentage of the purchase price or a flat dollar amount. The default of 2% bundles origination, title, escrow, and recording fees. Adjust up if agent commissions apply.

- Set the down payment percentage. The default is 25%. Total cash invested updates automatically as these inputs change.

Step 2: Set the loan terms

- The calculator assumes a 30-year fully amortizing DSCR loan for rental properties, one of the most common financing options for real estate investors. Enter the interest rate from a current loan quote or leave the default value as a baseline. You can check the current DSCR loan rates that we update daily.

Step 3: Enter rental income

- Enter monthly gross rent as the full market rent when occupied.

- Set the vacancy rate to account for time the unit sits empty between tenants. A 5% vacancy equals roughly three weeks per year.

Step 4: Enter operating expenses

- Property taxes and insurance are annual figures. Enter them from the actual tax bill and insurance quote.

- HOA is entered as a monthly dollar amount. Enter 0 if no HOA applies.

- Property management, maintenance, and CapEx reserve each accept either a percentage of effective gross income or a flat monthly dollar amount. Toggle between % and $ using the button next to each field. The converted value displays below each input in real time.

- Management defaults to 8%. Maintenance defaults to 5%, which covers ongoing small repairs. CapEx defaults to 0%. Add a reserve here for properties with aging roofs, HVAC, or major appliances.

Step 5: Read the results

- Monthly cash flow is the top output. A negative number means the property costs more per month than the net operating income (NOI) it generates after debt service. Adjust rent, down payment, or expenses to identify the break-even point.

- Cap rate measures a property's unlevered yield by dividing net operating income (NOI) by the purchase price. Because it excludes financing, it provides a consistent way to compare investment opportunities. If the cap rate is lower than the interest rate, borrowing reduces cash flow instead of improving returns.

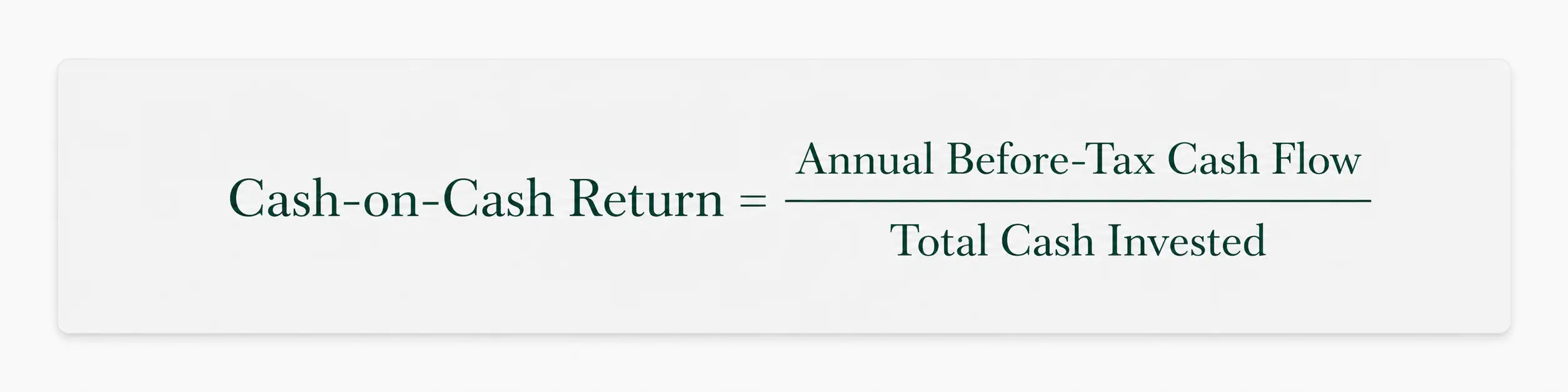

- Cash-on-cash return measures the annual return on the cash invested in a property after financing is considered. It shows how efficiently the investor's capital is working. A negative cash-on-cash return means the property requires additional cash each year rather than producing positive cash flow.

- DSCR shows whether the loan qualifies. Gross rent divided by full PITIA must exceed 1.0 for a DSCR loan to fund. A DSCR above 1.25 is considered strong.

Rental Property Profit Calculator: What Good Results Look Like

Most buy-and-hold investors target at least $100 to $200 per door per month in cash flow after every operating cost and the mortgage payment. A property that barely clears zero leaves no buffer for extended vacancy or an unplanned repair.

Cap Rate for a rental property

Cap rate (capitalization rate) measures a property's annual return before financing by dividing net operating income (NOI) by the purchase price. Because it excludes mortgage payments, it provides a consistent way to compare rental properties regardless of how they are financed. Like most underwriting metrics, cap rate is a snapshot based on current income and expenses. It does not account for future appreciation, rent growth, renovations, tax benefits, or changes in operating costs, so it should be used as a screening tool rather than a complete measure of investment performance.

Cap rates between 5% and 8% are common across many U.S. residential rental markets. Secondary markets often produce cap rates in the 6% to 10% range, while major metros typically trade between 3% and 5% as investors accept lower current yield in exchange for stronger long-term appreciation.

A higher cap rate is not automatically better. It often reflects greater risk, such as weaker demand, higher vacancy, slower appreciation, or elevated operating costs. Cap rate should always be evaluated alongside the property's cash flow, location, market fundamentals, and overall investment strategy.

Cash-on-cash return for rental property

Cash-on-cash return is one of the most widely used metrics for evaluating leveraged rental properties, but it should not be viewed in isolation. It measures the property's current cash yield based on today's income, expenses, and financing, making it a static snapshot rather than a long-term performance forecast. This calculator assumes rent, vacancy, property taxes, insurance, and other operating costs remain unchanged, so it does not estimate how future market conditions may affect returns.

Likewise, the calculation does not account for tax benefits, principal paydown, or future appreciation. Some investors prioritize immediate cash flow, while others accept lower initial returns in exchange for stronger long-term appreciation and equity growth realized at refinance or sale. Cash-on-cash return is an important screening metric, but it should be evaluated alongside the property's long-term investment strategy rather than used as a standalone measure of performance.

Cash-on-cash returns between 6% and 12% are a common target for leveraged buy-and-hold investments. The metric reflects the annual return on the investor's cash invested after financing is considered. A result below 5% leaves little margin for unexpected expenses or vacancies, while a negative return means the property is consuming cash rather than generating it.

How DSCR Connects to Loan Qualification

Cash flow, cap rate, and cash-on-cash return measure a property's performance for the investor. DSCR measures the same performance for the lender. It compares gross monthly rent to the full monthly housing payment (PITIA). That ratio determines whether the property's income supports the proposed loan. A property with strong cash flow typically clears the DSCR threshold. A property with thin margins often fails it.

When the ratio falls short, three adjustments typically move it: a larger down payment reduces the PITIA, a lower purchase price reduces the loan balance, or a stronger-rent property in the same market replaces the subject. For the full qualification criteria, see Ridge Street Capital's DSCR Loan Requirements.

Found a Deal That Works? Run It With Us.

Ridge Street Capital finances rental property acquisitions across 35 states. Submit property and borrower details through our Quick Application, and a loan officer reviews the numbers, proposed loan structure, and deal terms directly with you. Term Sheet delivered within 2 business hours. Get your loan Pre-Approval today.

Rental Property Profit Calculator FAQs

Can I use this calculator for a property I already own?

Yes. Enter the current market value in the purchase price field and your existing loan terms to evaluate the return on your current equity position. Use actual current rent and expense figures for the most accurate result. If you consider refinancing your property, use our DSCR refinance calculator.

Does this calculator work for 2–4 unit properties?

Yes. Enter the combined rent from all occupied units as the monthly gross rent. Apply a vacancy rate that reflects turnover across multiple units. The DSCR output represents the full property's rent-to-debt ratio, which is how most DSCR lenders underwrite small multifamily.

What vacancy rate should I enter if the property is about to be leased?

Use the market average for comparable rentals in the ZIP code rather than 0%. A 5% to 7% rate reflects realistic long-term performance for most well-located residential rentals. Properties in softer or high-turnover markets should model 10% or higher.

Does the calculator account for income taxes or depreciation?

No. The calculator produces pre-tax cash flow. Depreciation, mortgage interest deductibility, and rental income taxes each depend on the investor's filing status and ownership structure.

Why doesn't the calculator show a total ROI figure?

Cash flow and total ROI measure different things. Cash flow captures what a property produces now: income minus all costs in a given period. Total ROI adds appreciation, equity paydown from loan amortization, and the original capital invested, typically expressed as an annualized figure across a projected 5 to 10 year hold.

The calculator uses cap rate and cash-on-cash return rather than a long-term ROI metric. Both measure current performance with actual inputs. A total ROI projection requires forward-looking assumptions about future market values and appreciation that vary enough by market, property type, and hold period to make the output speculative rather than analytical. This calculator answers one question: does this property cash flow and qualify today?

What do operating expenses typically run on a rental property?

Operating expenses on a long-term rental commonly consume around half of gross rent before debt service. That ratio is the basis of the 50% rule: allocate 50% of monthly rent to taxes, insurance, maintenance, and management, and treat whatever remains as the pool available for mortgage payments and cash flow.

The ratio shifts by property and market. Check our article on the best states to buy rental properties in 2026. Lower-priced rentals in high-turnover areas tend to run above 50% due to higher vacancy frequency and maintenance demands. Higher-end properties in stable markets often come in below it.

The 50% rule works as a fast screen. A deal that fails it before the mortgage payment is likely to produce negative cash flow. A deal that passes it narrowly warrants a closer look in the calculator before committing.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)