Fix to Rent Loans: How to Finance the Buy, Renovate, and Hold Strategy

September 6, 2024

Most real estate investors understand the fix-and-flip model. Buy distressed, renovate, sell at a profit. Fix to rent is the same loan, but with a different exit, and that single difference changes how the entire deal needs to be evaluated.

Instead of selling at the end of a renovation, the investor refinances into a long-term DSCR rental loan and holds the property as a cash-flowing asset. The bridge loan gets paid off, the investor recovers a portion of their capital, and the property stays in the portfolio, generating rental income. When done correctly, the same capital funds the next deal.

This is the financing structure behind the BRRRR method. It works when the refinance exit is underwritten before the renovation starts, not evaluated for the first time after the rehab is complete.

What Is a Fix to Rent Loan?

You may have heard the term "fix to rent loan" and wondered: how is that different from a fix and flip loan?

The loan itself is the same product. Both are short-term, interest-only hard money loans structured around the property's After Repair Value (ARV), with a portion allocated to the purchase and a separate draw schedule funding the renovation budget. Fix to rent loans are business-purpose loans, meaning they fall outside conventional mortgage guidelines. The lender evaluates the asset, the rehab plan, and the projected ARV. Personal income, tax returns, and debt-to-income ratios are not part of the underwriting procedure.

The reason most lenders don't separate these products is that the underwriting analysis is the same. A lender evaluating a fix to rent deal checks whether the project makes sense as a sale and as a hold. A lender who runs the refinance test at origination will flag this before any capital is committed, and that conversation is far more useful to an investor than discovering the same problem after a renovation is complete.

Fix to Rent vs. Fix and Flip: Choosing the Right Exit

The hold exit makes sense when market rent produces a DSCR above 1.0 at 75% LTV, the ARV supports a loan large enough to recover most of the invested capital, and the investor's goal is portfolio growth rather than immediate liquidity.

The flip exit makes sense when the resale margin is strong, the investor needs full capital recovery to fund the next deal, or rental income at the projected ARV does not produce a viable DSCR. Some markets support strong ARVs but weak rent-to-value ratios. In those markets, selling is the better decision regardless of the investor's long-term goals.

The most disciplined fix to rent investors run both analyses before closing the acquisition. The deal should work as a flip if the hold does not come together as planned.

Exit strategy comparison:

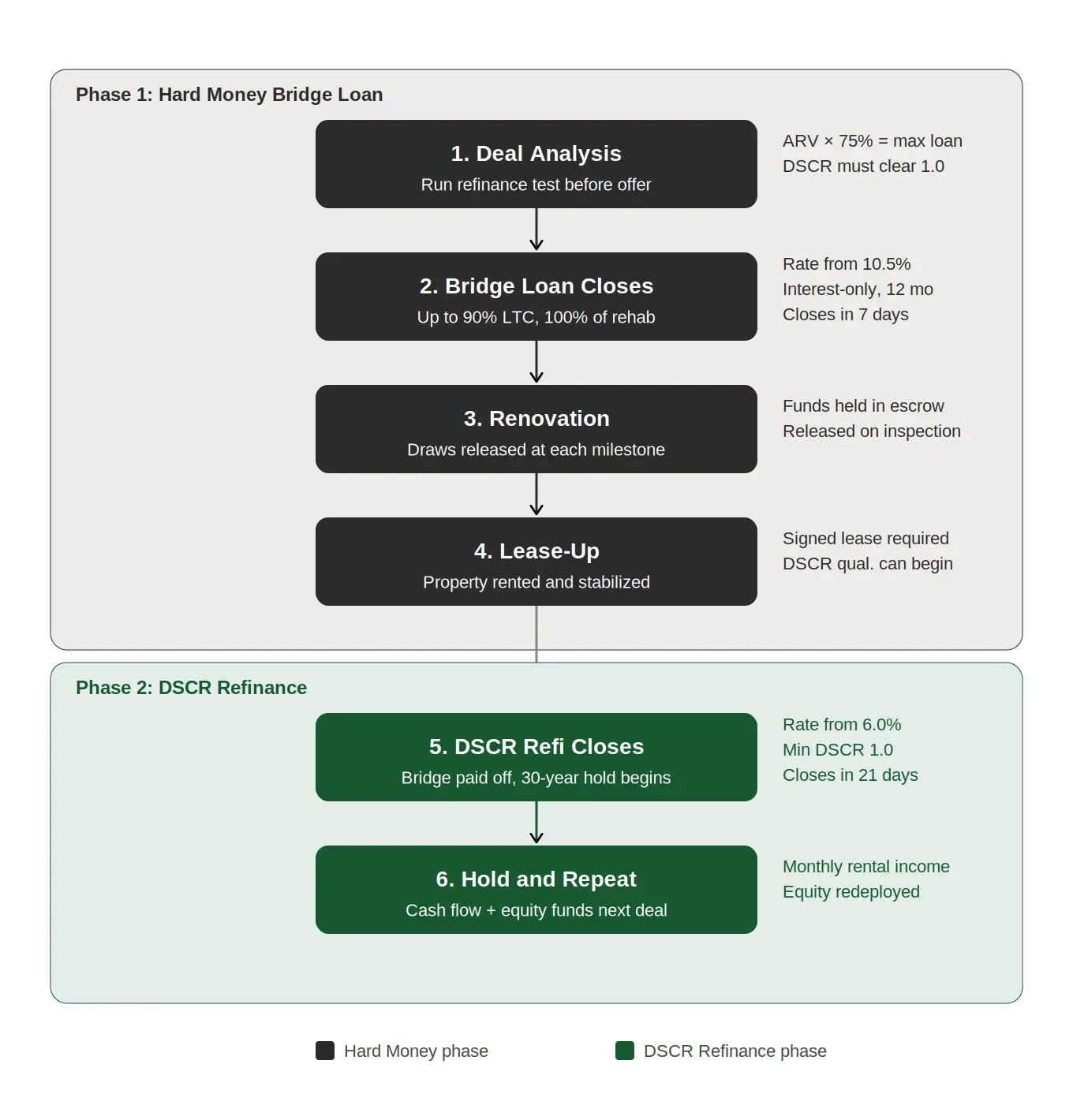

How the Two-Phase Financing Works

Fix to rent deals run on two separate loans. The bridge loan handles acquisition and renovation. The DSCR loan takes over once the property is stabilized and income-producing. Understanding each phase of the process helps investors avoid reaching the refinance stage with a completed renovation only to discover that the property's DSCR calculation does not support the planned exit strategy.

Phase 1: The Bridge Loan (Acquisition and Renovation)

The bridge loan funds the purchase and the rehab. Most programs cover up to 90% of the purchase price and 100% of the verified renovation budget, subject to a maximum of 75% of the After Repair Value. Payments are interest-only throughout the term, which keeps monthly carrying costs low while the renovation is underway. The bridge term is typically 12 months, sufficient for most rehab-to-stabilization timelines when the project is planned correctly.

Leverage at origination depends partly on experience. Borrowers with a documented track record of completed projects typically qualify for the upper end of available LTC. First-time borrowers can access competitive terms, but should expect leverage toward the lower end of the program range until their track record is established.

Renovation draws: Rehab funds are held in escrow at closing and released in draws as work is completed and verified. Borrowers submit draw requests with contractor invoices and progress documentation. Ridge Street Capital releases funds against the approved scope of work, with each draw tied to completed milestones rather than a fixed calendar schedule.

Phase 2: The DSCR Refinance (Long-Term Hold)

Once the renovation is complete and the property is leased, the investor refinances the bridge loan into a long-term DSCR rental loan. Qualification is based on the property's rental income relative to the new loan payment, not the borrower's personal income, tax returns, or portfolio size.

The DSCR loan is a separate underwriting event from the bridge loan. Working with a single lender for both phases means the property is already known: the lender has the appraisal, the title history, and the renovation documentation from Phase 1. The second underwrite focuses on confirming the stabilized rent, verifying the lease, and setting the final loan terms.

Seasoning: Most lenders require 6 months of ownership before a DSCR refinance based on the post-renovation value. At Ridge Street Capital, the seasoning requirement depends on what the refinance does. When the DSCR loan simply pays off the bridge loan balance with no additional cash proceeds, no seasoning is required. The renovation costs were documented and financed as hard costs through the original loan, which satisfies the standard rate-and-term condition. The investor can move to the DSCR loan as soon as the property is leased and stabilized. When the investor wants to pull equity above the bridge payoff, the transaction becomes a cash-out refinance, and a 6-month seasoning period applies.

Fix to Rent Loan Terms at a Glance

Here is the summary of the two phases' parameters for the fix-to-rent loan process at Ridge Street Capital.

The Refinance Test: What Lenders Evaluate at Origination

Before the bridge loan closes, a lender running the refinance test answers two questions. First: at the projected ARV, what is the maximum DSCR loan amount at 75% LTV? Second: at that loan amount, does the projected market rent produce a DSCR of 1.0 or above?

If the second question produces a failing number, the deal does not support the hold exit. The investor needs to know that before closing, not after 90 days of renovation. At Ridge Street Capital, when the numbers fall short, the team works through the adjustment with the investor: whether that means increasing the target market rent, tightening the renovation budget, or reconsidering the acquisition price. The goal is to structure a deal that works on both ends, not to simply fund the bridge loan.

Screening a market before committing to the hold strategy: Not every market supports the fix-to-rent exit at a given price point. A property with a strong ARV can still fail the DSCR test if local rents do not produce sufficient gross yield. As a starting benchmark, the gross rent-to-value ratio (monthly rent divided by the post-renovation value) should be at or above 0.7%. Below that threshold, the 75% LTV DSCR qualification math typically fails at minimum coverage.

When both questions produce acceptable answers, the investor enters the project knowing the exit works. The renovation can proceed on schedule without the DSCR qualification remaining an open variable.

A Real Deal: Fix to Rent in Mississippi

The example in Mississippi below shows how a fix to rent deal is structured across both phases, using a project financed through Ridge Street Capital.

Project parameters:

- Purchase price: $127,500

- Renovation budget: $40,000

- After Repair Value: $235,000

Phase 1 — Bridge Loan:

Phase 2 — DSCR Cash-Out Refinance:

The property is financed with a 30-year DSCR loan, and the rental income covers the full cost of mortgage, taxes, and insurance. The $36,040 invested in the deal came back as $23,075 in cash plus a cash-flowing asset with $58,750 in equity. That recovered capital funds the down payment on the next acquisition.

Who This Strategy Works For, and Who It Does Not

Fix to rent is the right structure for investors building a rental portfolio without deploying fresh capital on every acquisition. Each completed project recovers enough equity to fund the next down payment, which means the portfolio can grow without requiring proportional increases in invested capital.

Investors who fit this model have a 6-12 month project timeline and the capacity to carry a bridge loan through the renovation and lease-up. The returns on a fix to rent deal accumulate over years of cash flow and appreciation, not at a single closing.

Fix to rent does not work for investors who need immediate, full capital recovery. If the project budget is tight and the bridge loan cannot be serviced through a longer stabilization period, the pressure to sell increases.

Finance Both Phases with Ridge Street Capital

Not all investment property lenders are built to support fix to rent projects. The timing, underwriting, and execution requirements across both phases differ from a standalone bridge loan or a DSCR loan. A lender who does not understand both phases creates execution risk at the refinance stage.

Ridge Street Capital funds fix to rent deals across 35 states and underwrites both phases before the bridge loan closes. Every hard money loan we approve is evaluated against the planned DSCR refinance. If the numbers do not support the exit based on projected ARV and market rent, we flag it before closing, not after the renovation is complete.

If you're evaluating a fix-to-rent opportunity, start with a pre-approval. We'll review the numbers with you, evaluate the refinance exit, and help determine the financing strategy that best fits the property and your investment goals.

Fix to Rent Loans Frequently Asked Questions

What DSCR is required to qualify for the refinance?

As for loan requirements, the minimum DSCR at Ridge Street Capital is 1.0, meaning the monthly rental income must at least equal the full loan payment — principal, interest, taxes, and insurance. A DSCR above 1.0 improves pricing and provides a cash flow buffer against vacancy or expense increases. Run the DSCR calculation at 75% of your projected ARV before committing to a purchase price.

What credit score do I need?

The minimum credit score for both the bridge loan and the DSCR refinance is 660. Credit score affects pricing and leverage on both phases. The bridge loan is asset-based and places less weight on credit than conventional financing does, but the 660 minimum applies across the board.

Can I do this without prior renovation experience?

Yes. Experience is not a hard requirement for fix to rent loans at Ridge Street Capital. A detailed renovation budget, a clear project plan, and a realistic ARV estimate carry more weight than a renovation track record. First-time borrowers benefit from working with a general contractor who can produce a line-item scope before the loan application is submitted.

Can the property be held in an LLC?

Yes. Fix to rent loans are business-purpose loans and are routinely closed in the name of an LLC. The LLC entity must meet the standard credit and documentation requirements, and the guarantor must meet the 660 minimum FICO requirement. An LLC structure is often preferred for liability protection and tax treatment of rental income.

What happens if the DSCR refinance doesn't work at project completion?

If the property's rental income doesn't support a 1.0 DSCR at 75% LTV, the DSCR refinance either doesn't close or closes at a lower LTV, which reduces or eliminates the cash-out proceeds. The investor is left holding a bridge loan balance that needs to either be paid off, extended, or exited through a sale. This is why the refinance test at origination matters: running the DSCR numbers before closing the acquisition identifies whether the hold exit is viable before any capital is committed.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)