Turnkey Rental Properties: Costs, Returns & Financing

July 16, 2026

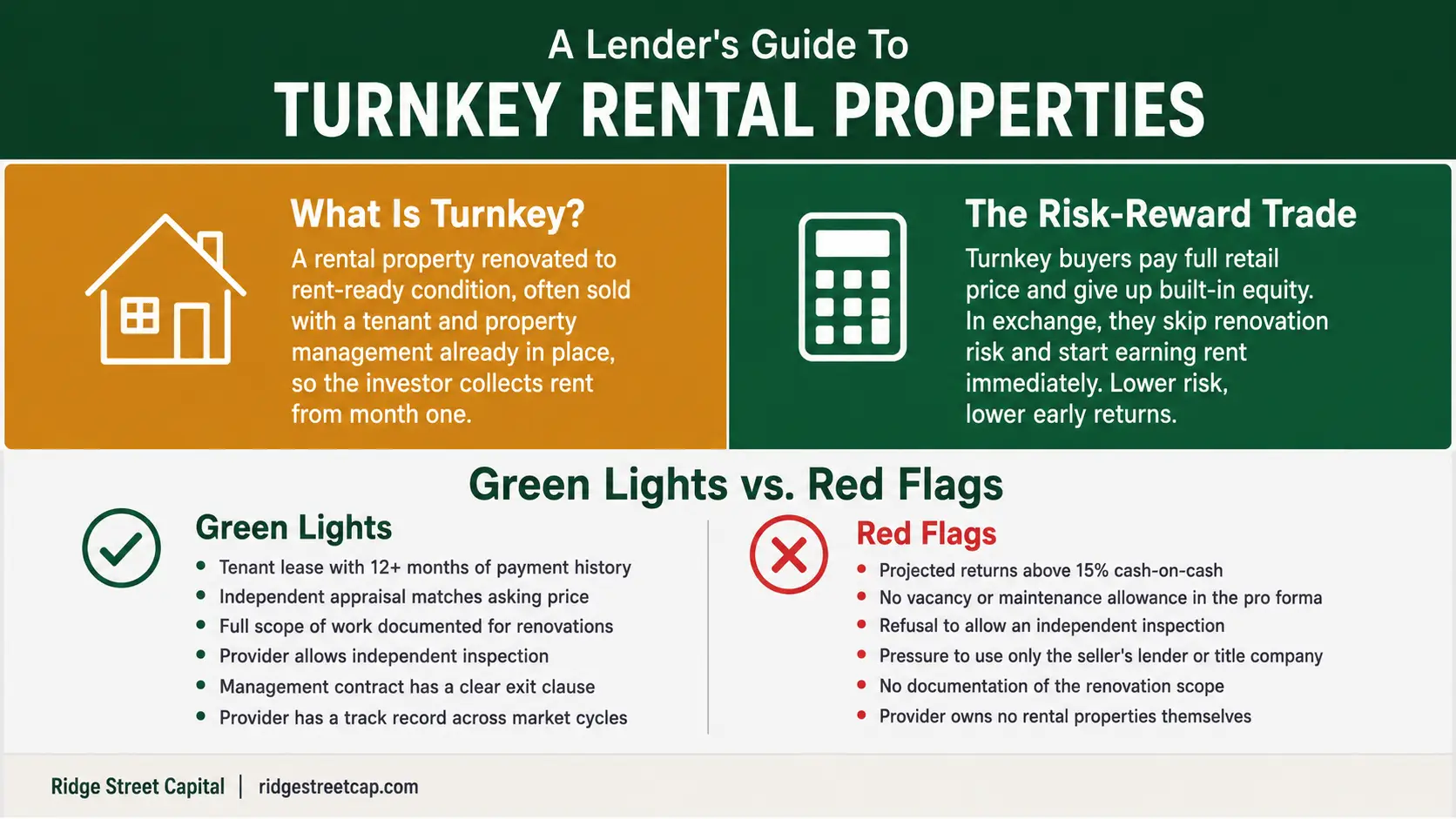

A turnkey rental property is a home that has been renovated or newly built to rent-ready condition, often sold with a tenant and property management already in place. The investor closes, takes over the lease, and collects rent from the first month of ownership.

The challenge is that “turnkey” has no fixed legal or industry definition. One seller may use the term for a fully renovated property with a tenant already in place. Another may use it for a cosmetic flip with fresh paint but aging plumbing, electrical, or mechanical systems.

This guide explains how the turnkey model works, who earns money at each step, what the numbers look like once every expense is counted, and how investors finance these purchases.

Ridge Street Capital underwrites rental property loans in 35 states and reviews turnkey pro formas as part of that work.

What Is a Turnkey Rental Property?

A turnkey rental property is an investment property sold in rent-ready condition. In most cases, the property should not need major repairs or renovations before a tenant can occupy it.

Some turnkey properties already have a tenant in place and a property management company handling day-to-day operations. That can help the buyer step into an income-producing asset more quickly, but the investor still needs to verify the lease, tenant quality, property condition, and operating expenses before closing.

In practice, sellers apply the term to three different products:

A property with a tenant in place and 12 months of payment history is usually stronger than a vacant rent-ready property because the rental income is already documented.

The rule is simple: do not rely on the label. Review the purchase contract, lease, tenant payment history, and management agreement to confirm what is actually being sold.

How Does the Turnkey Model Work?

With the definition established, the next question is how these properties reach the market. A turnkey operator usually buys a distressed or off-market property, renovates it, places a tenant, sets up management, and sells the finished rental to an investor.

The operator earns money in three places:

- The acquisition-to-sale spread: the difference between what the operator paid plus renovation cost and what the investor pays. This spread commonly ranges from $20,000 to $60,000 per property, depending on the market.

- Ongoing management fees: most providers keep the property under their in-house management after the sale, typically at 8% to 10% of collected rent plus leasing fees of half to one full month's rent per new tenant.

- Referral relationships: some providers earn fees for steering buyers toward affiliated lenders, insurance agents, or closing companies.

A turnkey operator earns a margin when the operator removes real execution risk from the investor.

The problem starts when the seller uses a pro forma to make the deal look stronger than it is. Four line items go missing from seller pro formas more than any others: a vacancy allowance, a maintenance budget, capital reserves for large replacements such as a roof or HVAC system, and leasing fees for future tenant turnover.

A Sample Turnkey Deal With Every Expense Counted

The trade-off becomes concrete with real numbers. Consider a turnkey single-family home in a mid-sized Southeast market, purchased with a 30-year fixed rental loan at an example investment property mortgage rate of 7%.

At 20% down and a 7% rate, this deal breaks even on monthly cash flow once every real expense is counted. That result surprises many first-time buyers, because the seller's pro forma for the same property often shows $250 to $400 in monthly cash flow. The difference is the vacancy, maintenance, capital reserve, and management lines.

Breakeven cash flow does not make the deal worthless.

The tenant pays down the loan principal, which builds roughly $1,300 to $1,400 of equity in the first year on this loan size. Rents in most markets rise over time while the loan payment stays fixed. Depreciation deductions shelter a portion of the rental income from taxes. An investor who puts 25% down instead of 20% turns the same property cash-flow positive at about $59 per month. Combined with principal paydown, that investor earns roughly 4% on invested cash before any appreciation or rent growth.

Investors should also account for reserve requirements on rental property loans. Many investment property lenders require reserves equal to several months of PITIA, which includes principal, interest, taxes, insurance, and HOA dues. A common requirement is six months, but the exact amount depends on the loan program and borrower profile. At closing, the investor may also need to fund escrow deposits for property taxes and insurance. These are not operating expenses, but they do increase the cash needed to close.

Investors can run these numbers on any property with the Ridge Street Capital rental property profit calculator.

Pros and Cons of Turnkey Rental Properties

The sample deal shows both sides of the strategy at once. Here is the full picture in summary form.

Advantages

- Income from day one: a tenanted property produces rent in month one, where a renovation project produces nothing for 2-6 months.

- No renovation risk: the buyer never faces contractor delays, budget overruns, permit problems, or rehab loans, which sink a measurable share of first-time renovation projects.

- Access to distant markets: professional management makes ownership practical from any state, so investors in high-cost metros can buy where prices and rents actually work.

- Lower early maintenance: new systems and finishes push major repair costs years into the future, and some new-build components carry warranties.

- A managed entry point: first-time investors learn ownership without simultaneously learning construction and leasing.

Drawbacks

- Full retail pricing: the buyer starts with little or no equity, and the provider's margin of $20,000 to $60,000 sits inside the purchase price.

- No forced appreciation: the seller has already captured the renovation value, so returns depend on cash flow, loan paydown, and market appreciation alone.

- Dependence on the manager: an out-of-state owner experiences the property entirely through the management company, and a weak manager erodes returns.

- Inflated projections: Seller pro formas can make returns look stronger by omitting key operating costs.

- Thin year-one cash flow: at current rates and 20% down payment, many turnkey deals hover near breakeven until rents grow.

Who Should Buy a Turnkey Rental Property?

The pros and cons above follow one principle that runs through all of real estate investing: returns are payment for risk carried and work performed. A turnkey purchase transfers both to the provider. The provider absorbs the renovation risk, the contractor problems, the permit delays, and the leasing risk, and delivers a stabilized asset. The buyer pays for that transfer through the retail price and accepts a lower return ceiling in exchange.

This trade explains the return profile in the sample deal above in this article. A renovation investor might earn 15% to 25% on a project because those returns compensate for the months of carrying costs, the budget overruns, and the deals that fail outright. A turnkey buyer earns single-digit cash returns in year one because almost nothing can go wrong in year one.

Lower risk pays less.

The comparison only becomes unfair when a buyer pays turnkey prices and still carries renovation-grade risk, which is exactly what happens with a repainted flip sold under the turnkey label.

Seen through that lens, turnkey purchases fit investors who have capital and lack time: professionals with demanding careers, owners diversifying across several markets, residents of expensive metros where local properties cannot produce rent that covers the mortgage, and first-time buyers who want professional management from the start.

For these investors, the provider's spread is the price of converting capital into income without converting their schedule into a second job.

Investors whose returns come from the work itself sit outside the model. An investor who renovates well earns the provider's spread instead of paying it, and is paid for the risk the turnkey buyer avoids.

An investor who needs equity at closing to refinance and repeat, the core mechanic of the BRRRR method, cannot get it from a retail-priced purchase. Hands-on owners who want control over finishes, tenant selection, and repairs will find the turnkey managed structure restrictive rather than convenient.

How to Evaluate a Turnkey Property and Provider

For investors who fit the profile, the next step is to verify the deal. These six checks help determine whether the purchase is actually sound.

- Order an independent inspection. A renovated property still requires a full inspection from an inspector the buyer hires directly. The inspection confirms whether "fully renovated" means new systems or new paint.

- Verify the value. An appraisal or a broker price opinion establishes what the property is worth without the turnkey label. Buyers should pay no more than appraised value, and a lender's appraisal provides this check at no extra effort during financing.

- Audit the lease. Request the signed lease, the tenant's payment history, and confirmation that the security deposit transfers at closing. A lease signed two weeks before listing deserves more scrutiny than one with a year of on-time payments.

- Rebuild the pro forma. Add the missing line items: 5% vacancy, 5% maintenance, 5% capital reserves, actual management and leasing fees, and a fully amortizing loan payment.

- Read the management contract. Confirm the monthly fee, the leasing fee, the markup on repairs, the contract term, and the termination clause.

- Vet the provider. Look for a track record across full market cycles, principals who own rentals themselves, written scopes of work for each renovation, and consistent third-party reviews on platforms.

Red flags include projected cash-on-cash returns above 15%, refusal to allow an independent inspection, pressure to use the seller’s lender or title company, and missing documentation for the renovation scope.

How to Finance a Turnkey Rental Property

Due diligence confirms the asset. Financing shows whether the numbers still work after the loan is added.

For most turnkey rentals, the monthly payment is one of the largest expenses. The interest rate, loan amount, reserves, and closing costs can all change the investor’s cash flow and cash-on-cash return.

Why DSCR Loans Fit Turnkey Purchases

Most turnkey buyers finance with DSCR loans. DSCR stands for debt service coverage ratio: the property's monthly rent divided by the full monthly payment of principal, interest, taxes, insurance, and any HOA dues. A property renting for $1,650 with a $1,253 total payment carries a DSCR of 1.32, meaning the rent covers the payment 1.32 times over.

The lender approves the loan based on that ratio rather than on the borrower's personal income, so DSCR loans require no tax returns, no W-2s, and no employment verification. For turnkey properties specifically, the structure fits because the income evidence already exists: a transferring lease with payment history is the strongest documentation a rental property can offer. Full requirements are covered in the Ridge Street Capital DSCR loan requirements guide.

DSCR vs. Conventional Loans for Turnkey Rentals

Conventional investment mortgages remain an option, and the two products suit different borrowers.

Conventional financing works when the investor has strong W-2 income, a low debt-to-income ratio, fewer than ten financed properties, and no need for LLC ownership. Investors who are self-employed, scaling past the property cap, or buying inside an entity move to DSCR loans, and most turnkey portfolios end up there. Check the full guide on DSCR loans vs. Conventional Loans.

Financing a Turnkey Purchase With Ridge Street Capital

At this point the work is done in the right order: the property is verified, the pro forma is rebuilt, and the numbers hold. Financing is the step that turns that analysis into an owned, income-producing asset.

Ridge Street Capital is a direct private lender specializing in rental and investment property loans across 35 states. Investors submit the address and basic deal terms, and receive a term sheet within 2 business hours. Most DSCR purchase loans close in 21 to 25 days, inside a standard closing window on a tenanted turnkey sale.

Turnkey Rental Property Frequently Asked Questions

Are turnkey rental properties worth it?

A turnkey purchase is worth it when the verified numbers work: the price matches the appraisal, the rebuilt pro forma shows the property covering all expenses, and the buyer's goal is income with minimal time rather than equity creation.

Are turnkey properties overpriced?

Some are. Providers sell at full retail value, and weaker providers price above it, counting on out-of-state buyers who do not know the market. The protection is simple: order an appraisal and pay no more than the appraised value.

Do turnkey properties come with tenants?

Not always. The term covers vacant rent-ready homes, managed homes awaiting a tenant, and fully tenanted homes. Confirm in the purchase contract that the lease, the payment history, and the security deposit all transfer at closing.

Can you buy a turnkey rental with a DSCR loan?

Yes, and the fit is natural because DSCR lenders qualify the loan on rental income. An in-place lease documents that income directly. Expect 20-25% down and a minimum credit score around 660 with most programs.

Can a turnkey rental property work as a 1031 exchange replacement?

Yes, and turnkey properties are one of the most common replacement choices in a 1031 exchange. A rent-ready property with a tenant already in place removes the renovation timeline that would otherwise strain the exchange's 45-day identification window and 180-day closing deadline. Investors financing this kind of purchase can review the requirements and timelines in Ridge Street Capital's 1031 exchange loan guide.

Where should investors buy turnkey rental properties?

Market selection matters more for turnkey purchases than for local rentals, since the whole strategy depends on buying where rents, prices, and property management are strong even when the investor lives elsewhere. Turnkey providers concentrate in a handful of landlord-friendly, cash-flow-positive markets for exactly this reason. Ridge Street Capital's guide to the best states to buy rental property breaks down which markets currently fit that profile.

Funding For Purchase + Rehab

$50,000 up to $3,000,000

Interest Rate 10.5%-11.5%

Origination Fee From 1.5%

Up to 90% of Purchase and 100% of Rehab

Perfect for first-time investors or experienced investors scaling their rental portfolio.

.png)

.png)

Designed for investors pursuing higher rents with a short term rental strategy.

.svg)